- WFRP (Whole-Farm Revenue Protection) covers all commodities on your farm under one policy — including specialty crops

- Maximum insurable revenue is $8.5M for most farms

- You need 5 consecutive years of IRS Schedule F returns to qualify

- Diversification discount: more commodity types = lower premium

- WFRP replaces all individual APH policies on your farm — you cannot carry both

What WFRP Covers and Doesn't Cover

WFRP insures the total revenue of your entire farm operation against unexpected revenue loss due to natural causes, market disruptions, or other covered events. The policy covers all commodities you produce and sell — grains, livestock, specialty crops, vegetables, and orchard crops can all be included under a single policy.

— USDA Risk Management Agency — WFRP Policy

- Whole-Farm Revenue Protection (WFRP)

- A single crop insurance policy that covers total farm revenue across all commodities, based on your 5-year Schedule F average.

- Diversification Discount

- A premium reduction for farms growing multiple commodities: 10% for 2, 20% for 3, 30% for 4, up to 50% for 5 or more.

- Olympic Average

- A 5-year average that drops the highest and lowest years, used to calculate your WFRP revenue guarantee.

Pros

- Covers your entire farm operation under one policy — up to

$8.5M in insurable revenue - Diversification discount: up to 50% off premiums for farms with 5+ commodities

- Replaces all individual APH policies, simplifying coverage management

- Covers specialty crops, organic production, and direct-market revenue that standard policies miss

- Uses 5-year Schedule F average — smooths out single-year disasters in your baseline

Cons

- Requires 5 consecutive years of Schedule F tax records — new farms cannot qualify

- January 31 sales closing date is earlier than most individual crop policies

- Complex policy structure — harder to understand and manage than standard RP

- Revenue decline must hit the whole farm, not just one crop, to trigger payment

- Not cost-effective for single-commodity operations without the diversification discount

Who This Is For

Diversified farms growing 3 or more commodities — especially specialty crop growers, organic operations, and farms with significant direct-market sales. WFRP is designed for operations where standard single-crop policies leave coverage gaps.

Who Should Look Elsewhere

Single-crop corn or soybean farms should stick with Revenue Protection (RP) — it is simpler, better understood by agents, and does not require 5 years of Schedule F history. New farms without 5 years of tax records cannot qualify for WFRP.

Watch this USDA explainer video:

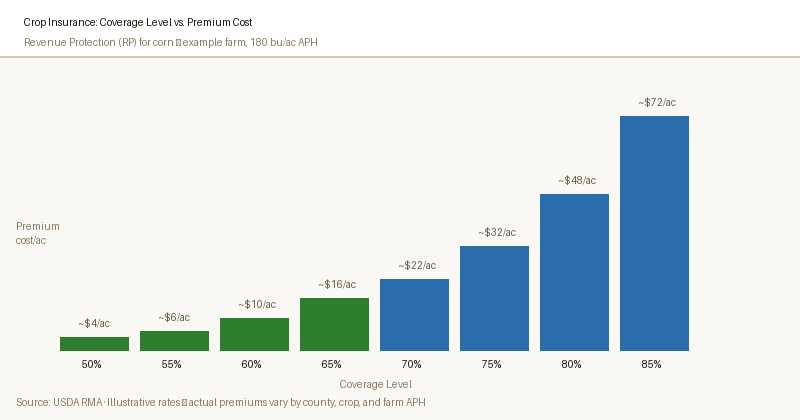

The insured revenue is set using your allowable revenue, calculated from your most recent five years of Schedule F tax returns. Coverage levels range from 50% to 85% of your allowable revenue in 5-percentage-point increments.

What WFRP Covers

- All crops and commodities grown and sold on the insured farm

- Livestock and livestock products (within limits)

- Specialty crops, organic crops, and diversified vegetable operations

- Revenue losses due to natural causes (drought, flood, hail, disease)

- Revenue losses due to low prices when combined with yield loss

What WFRP Does Not Cover

- Price declines alone (without a corresponding yield loss trigger)

- Farming operations with fewer than

5 yearsof Schedule F history - Revenue above the

$8.5Mmaximum insurable amount - Farms where more than 50% of revenue comes from a single commodity (a separate individual policy is recommended in those cases)

- Off-farm income or custom work revenue

Who Benefits Most from WFRP

WFRP was designed specifically for operations that are poorly served by individual crop policies.

If you grow multiple commodities, rotate crops significantly, or raise specialty crops that lack their own Actual Production History (APH) policies, WFRP is likely the more cost-effective and comprehensive choice.

WFRP is the strongest fit for:

- Diversified operations with 3 or more commodities — the diversification discount significantly reduces premiums

- Organic farmers — WFRP recognizes organic price premiums in the revenue calculation

- Specialty crop growers (vegetables, fruits, herbs, ornamentals) — many specialty crops have no individual APH policy available

- Farms with significant crop rotation — WFRP covers whatever you grow, regardless of how your mix changes year to year

- Direct-market farms and CSA operations — farm revenue is captured holistically through Schedule F, not estimated per crop

How WFRP Revenue Is Calculated

Your allowable revenue under WFRP is based on the Olympic average of your last five years of Schedule F net income, adjusted for farming operations expenses and income categories.

RMA actuaries calculate a "farm revenue history" figure that represents what your operation is expected to produce in a normal year.

Here is how the calculation works step by step:

- Gather five consecutive Schedule F returns — these must be the five most recent years for which tax returns have been filed

- Identify gross farm revenue — RMA uses total farm income from Schedule F, not net income

- Apply the Olympic average — drop the highest and lowest year; average the remaining three

- Multiply by your elected coverage level — 50% to 85% in 5-point increments

- The result is your revenue guarantee — if actual farm revenue falls below this threshold, an indemnity is triggered

If actual farm revenue in the policy year falls below the revenue guarantee, you receive an indemnity payment equal to the shortfall (up to your maximum insured amount).

The Diversification Discount

One of WFRP's most powerful features is the diversification premium discount. The more distinct commodity types you produce, the lower your premium — because a diversified farm is statistically less likely to experience total revenue failure across all commodities simultaneously.

| Number of Commodities | Premium Discount | Notes |

|---|---|---|

| 1 commodity | No discount | Single commodity — limited WFRP benefit |

| 2 commodities | Up to 10% | Modest diversification recognized |

| 3 commodities | Up to 20% | Meaningful discount begins here |

| 4 commodities | Up to 30% | Strong diversification benefit |

| 5+ commodities | Up to 50% | Maximum discount — specialty crop farms often qualify |

Discount percentages are approximations based on RMA actuarial tables. Actual discounts depend on commodity types, revenue mix, and historical variability. Ask your crop insurance agent for a farm-specific quote.

How WFRP Compares to Individual Crop Policies

| Feature | WFRP | Individual APH/RP Policies |

|---|---|---|

| What's covered | All commodities on the farm | One crop per policy |

| Revenue basis | Schedule F farm revenue history | Per-acre yield and price |

| Best for | Diversified, specialty crop, organic farms | Single commodity, high-acreage row crop farms |

| Specialty crops | Yes — included automatically | Limited; many have no individual policy |

| Diversification discount | Yes — up to 50% | No |

| Organic premium recognition | Yes | Limited; separate organic factors apply |

| Can hold simultaneously | No — replaces individual policies | Yes — multiple crops |

| Required documentation | 5 years Schedule F, farm records | Production records per crop |

| Sales closing date | January 31 | Varies by crop and county |

How to Buy WFRP

WFRP is available exclusively through USDA Risk Management Agency (RMA)-approved crop insurance agents. It is not available directly through the USDA or FSA (Farm Service Agency) — you must work with a private agent who is certified to sell WFRP policies.

The annual sales closing date for WFRP is January 31 for the upcoming crop year. Missing this deadline means waiting another full year — plan your application in November or December to allow time for document gathering and agent review.

Documents You'll Need

- Five consecutive years of IRS Schedule F (Profit or Loss from Farming)

- A farm map showing all fields, acreage, and commodity types

- Your Farm Serial Number (FSN) from your FSA farm record

- Commodity production and marketing records from the most recent year

- Organic certification documentation (if applicable)

Find a WFRP-approved agent at rma.usda.gov

The RMA Agent Locator tool lets you search for certified WFRP agents by zip code. Not every crop insurance agent is certified to sell WFRP — verify your agent's WFRP certification before scheduling an appointment. Find an agent at rma.usda.gov →

Is WFRP Right for You? Decision Checklist

Use this checklist to determine whether WFRP is the best fit for your operation. If you check 3 or more of these boxes, WFRP is worth a detailed quote comparison against your current individual policies.

- I grow 3 or more distinct commodity types on my farm

- I grow specialty crops, vegetables, fruits, or herbs

- I am certified organic or transitioning to organic production

- My crop mix changes significantly from year to year due to rotation

- I sell through direct markets, farmers markets, or a CSA

- I have 5 or more consecutive years of Schedule F tax returns

- My total farm revenue is below

$8.5Mannually - I find managing multiple individual crop insurance policies time-consuming