Pros

- FSA Down Payment program: 5% down, FSA covers 45% at 3% — the most affordable path to land ownership

- Beginning farmers get priority processing and dedicated FSA set-asides

- State programs (IADA, RFA, IFDA) stack with FSA for even lower effective rates

- No minimum credit score for FSA Direct — they evaluate your full financial picture

- Up to 100% financing available for qualifying beginning farmers through FSA

Cons

- Must have fewer than 10 years of farming experience to qualify as "beginning"

- FSA programs have loan caps (

$600KDirect) that may not cover prime farmland - State programs have limited annual funding — first-come, first-served

- Application process requires extensive documentation and farm business plan

- Beginning farmer status expires after 10 years regardless of farm size

Who This Is For

First-generation farmers, career changers entering agriculture, and anyone with fewer than 10 years of farming experience. Especially valuable for aspiring farmers with limited savings who need the 5% down payment path to land ownership.

Who Should Look Elsewhere

Farmers with more than 10 years of experience no longer qualify as "beginning farmers" under FSA rules. Established operations should apply for standard FSA Direct or Farm Credit loans instead.

— USDA Farm Service Agency

Who Is a Beginning Farmer? (FSA Definition)

Watch this USDA explainer video:

The USDA Farm Service Agency has a specific legal definition for "beginning farmer" that determines eligibility for priority loan programs. Under FSA rules, a beginning farmer is someone who:

- Has not operated a farm for more than 10 years

- Has not been the sole owner of a farm for more than 10 years

- Will operate as a family-size farm after the loan closes

- Meets all standard FSA loan eligibility criteria (citizenship, legal capacity, no outstanding federal judgments)

The 10-year clock runs from the date you first began farming as an operator — not from when you were a child working on your parents' farm.

Supervised experience as an employee doesn't count toward the 10 years. Veterans with military service may qualify for additional programs through the FSA Veterans Beginning Farmer loan set-aside.

FSA Beginning Farmer Loan Programs

FSA Farm Ownership Direct — Beginning Farmer Priority

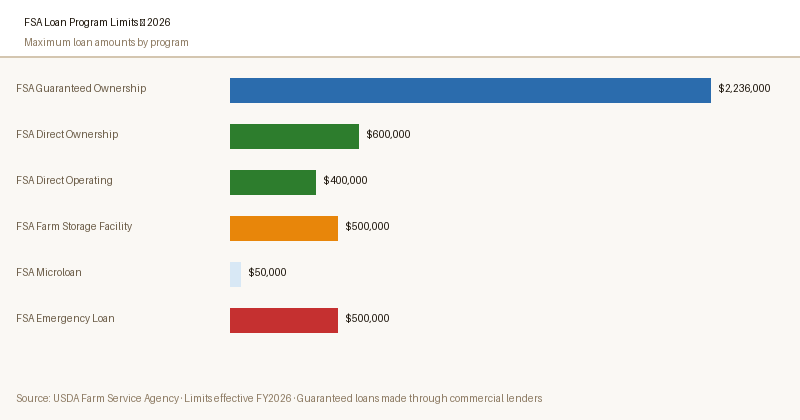

Beginning farmers receive priority consideration for FSA Direct Ownership loans. Rate: 4.75% as of May 2026. Maximum: $600,000. Term: up to 40 years.

Required down payment for the standard direct program varies, but beginning farmers may be eligible for as little as 5% down through the Down Payment Loan program (see below).

FSA Down Payment Loan Program

This specialized program allows beginning farmers and socially disadvantaged farmers to purchase farmland with as little as 5% down. The loan structure works as follows:

- You contribute 5% of the purchase price as a down payment

- FSA provides 45% of the purchase price as a direct loan at a reduced rate (currently 3% for the FSA portion, May 2026)

- A commercial lender or the land seller provides the remaining 50% as a subordinate loan

- Total financing: 95% of purchase price

The FSA portion is capped at $300,000 and has a maximum term of 20 years. The reduced 3% rate on the FSA portion makes this the most affordable land purchase option available for beginning farmers with limited capital.

FSA Direct Operating Loans — Beginning Farmer

FSA Operating loans (maximum $400,000, 5.25% as of May 2026) also give priority to beginning farmers. For new growers who need seed, fertilizer, and input capital before their first harvest, FSA operating loans provide the lowest-cost working capital available.

The Microloan sub-program ($50,000 maximum) has a simplified application ideal for very small operations just getting started.

USDA FSA Beginning Farmer Programs — No Affiliate Relationship

Apply for FSA Beginning Farmer loans at fsa.usda.gov. Call your local service center to ask specifically about beginning farmer priority dates and fund availability for your county.

State Beginning Farmer Programs

Most agricultural states maintain their own beginning farmer loan programs that can supplement or work alongside FSA loans. These programs often offer below-market interest rates, down payment assistance, or loan participation with local lenders.

| State | Program | Max Amount | Rate Feature | Website |

|---|---|---|---|---|

| Iowa | Beginning Farmer Loan Program (IADA) | $345K+ | Below-market rate | agdevelopment.iowa.gov |

| Minnesota | Rural Finance Authority (RFA) | $950K | 2% below market | mn.gov/deed |

| Illinois | IFDA Beginning Farmer Program | $575K | Below-market bond rate | ifda.com |

| Kansas | Kansas Rural Finance Authority | $500K | Participation loan | krfa.ks.gov |

| Wisconsin | DATCP Beginning Farmer Programs | Varies | Tax credits + loans | datcp.wi.gov |

| Nebraska | Neb. Investment Finance Authority | $500K | Below-market rate | nifa.org |

Down Payment Assistance

Beyond the FSA Down Payment program, beginning farmers can access down payment assistance from several sources:

- State Ag Finance Authorities — As shown in the table above, most corn belt and plain states have programs that provide low-interest secondary financing that supplements FSA or commercial first mortgages

- Land-grant university extension programs — Some states offer educational requirements that unlock lower-rate financing; completing an approved farm business planning course can qualify borrowers for better terms

- Vendor/seller financing — Many retiring farmers are willing to carry a seller note for part of the purchase price, effectively filling the gap in the FSA Down Payment program structure

- USDA Rural Development — Separate from FSA, USDA Rural Development offers housing loans and some agricultural business programs that may supplement farm purchase financing

Commercial Options for Beginning Farmers

When FSA timelines don't work — or when your operation needs capital faster than government programs allow — commercial lenders can bridge the gap.

Lendio — Best Marketplace for Thin Credit

Beginning farmers often have limited formal credit history outside of student loans or personal credit cards. Lendio's marketplace model presents your application to 75+ lenders simultaneously, surfacing options from lenders who specialize in limited-credit-history borrowers.

For operating capital needs of $10K–$250K, Lendio can identify options where traditional banks cannot. The tradeoff is rate: marketplace rates for thin-credit borrowers start around 8–12% for term loans.

National Funding — When FSA Isn't Fast Enough

If you have a land opportunity that needs to close in 30 days, or you need planting capital before an FSA decision comes through, National Funding offers operating loans up to $500K with approvals in 24 hours.

The rate premium over FSA is real (7.00%+ vs. 5.25%), but the speed may be the only option for time-sensitive situations. Many beginning farmers use National Funding as a bridge while their FSA application processes, then refinance with FSA once approved.

Can't Wait for FSA? Get Commercial Funding Today

National Funding approves beginning farmer operating loans in 24 hours. Lendio's marketplace surfaces options even with limited credit history. Both are no hard pull to see initial rates.

Common Mistakes New Farmers Make When Applying

- Applying too late. FSA processing takes 30–60 days. Beginning farmers who need capital for spring planting and apply in March face a race against the calendar. Apply in November or December for the following year.

- Not preparing a written farm business plan. FSA loan officers and commercial banks both want to see that you've thought through production costs, expected yields, and realistic income projections. A one-page farm business plan dramatically improves approval odds.

- Overlooking state programs. Most beginning farmers don't know their state has a below-market loan program that can stack on top of FSA. Check your state ag development authority before accepting any commercial offer.

- Using personal credit cards for farm inputs. Revolving credit card balances hurt your credit score and signal poor cash management to lenders. Farm operating loans — even at higher commercial rates — are better than credit card debt for input costs.

- Not securing crop insurance before applying. FSA and most commercial lenders require crop insurance evidence. Having your insurance agent lined up before you apply accelerates every other part of the process.

Frequently Asked Questions

What qualifies as a "beginning farmer" for FSA loan priority?

Can I get a farm loan with no farming experience?

What is the FSA Beginning Farmer Down Payment program?

$300,000 and has a maximum term of 20 years. The combined loan covers 95% of the purchase price, making it the most accessible land purchase program in the U.S. for new agricultural operators.Do I need good credit to get a beginning farmer loan?

Can I buy a farm with an FHA or conventional mortgage?

Are there beginning farmer loans for specialty crop or organic farms?

$50,000) is particularly well-suited for smaller specialty crop and direct-market beginning farmers who don't need the larger loan amounts of the standard programs.How long do I have before I lose my "beginning farmer" status?

Sources

- USDA Farm Service Agency — Beginning Farmer Loan Programs, verified May 2026

- Iowa Agricultural Development Authority — Beginning Farmer Program details, 2026

- Minnesota Rural Finance Authority — Beginning Farmer Program, 2026

- USDA Economic Research Service — Beginning Farmers and Ranchers: Financial Challenges, 2024