Pros

- AgDirect starting rates from 5.90% — lower than most commercial alternatives

- Section 179 allows full deduction (up to

$1,160,000) in the purchase year - Equipment itself serves as collateral — no additional real estate lien required

- Used equipment up to 15 years old can be financed at most agricultural lenders

- Dealer financing through AgDirect simplifies the purchase process

Cons

- Equipment depreciates — unlike land, it loses value while you still owe on it

- Minimum credit scores (600–660) exclude some beginning farmers

- Used equipment rates (6.50–9.50%) are notably higher than new equipment

- Maximum terms of 7–10 years create higher monthly payments than land loans

- Bonus depreciation drops to 20% in 2026 — tax benefits are declining

Who This Is For

Farmers buying tractors, combines, planters, hay equipment, grain bins, or other capital equipment who want to spread the cost over 3–10 years while claiming tax deductions in year one. Works best with 640+ credit and equipment valued at $5K+.

Who Should Look Elsewhere

Farmers who use equipment fewer than 500 hours per year should consider leasing instead — lower payments and easier upgrades. For equipment under $50K, an FSA (Farm Service Agency) Microloan at 5.25% may be cheaper than dealer financing.

Types of Agricultural Equipment Loans

Equipment financing for farms comes in three primary structures, each suited to different purchase situations and cash flow needs.

- Section 179 Deduction

- An IRS provision allowing you to deduct the full purchase price of qualifying equipment in the year you buy it, up to $1,160,000 (2026 limit).

- Bonus Depreciation

- An additional first-year depreciation deduction on new and used equipment. Phases down to 20% in 2026 and 0% in 2027.

- Point-of-Sale Financing

- Equipment financing arranged through the dealer at the time of purchase, typically offered by AgDirect through 1,300+ partner dealers.

Term Loan (Equipment Loan)

The most common structure: you borrow the equipment purchase price (minus any down payment), take title immediately, and repay over a fixed term of 3–10 years. Interest rates are fixed or variable.

At the end of the term, you own the equipment free and clear. This is the right structure when you plan to keep and use the equipment through its productive life and want to build equity in the asset.

Equipment Line of Credit

A revolving credit facility sized to your expected equipment purchases over 12–24 months. You draw against the line as you make purchases, converting each draw to a term note. Useful for dealers who are constantly buying and selling, or for operations that make frequent smaller equipment purchases. Farm Credit and some commercial banks offer equipment lines to established agricultural operations.

— Farm Credit Administration

Equipment Lease

You pay to use the equipment without owning it — similar to a vehicle lease. Operating leases keep equipment off your balance sheet and offer the option to return or upgrade at lease end. Finance leases (also called capital leases) are structured like loans with a $1 buyout option at the end.

Leasing is best when you need the latest technology, your operation is growing and uncertain about long-term equipment needs, or when depreciation limits make ownership less tax-advantaged.

Equipment That Qualifies

Virtually all productive agricultural equipment qualifies for farm equipment loans. Common categories include:

- Tractors — Row crop tractors, utility tractors, compact tractors, 4WD articulated tractors

- Combines and harvesting equipment — Grain combines, cotton pickers, corn heads, grain carts

- Planting equipment — Planters, drills, air seeders, transplanting equipment

- Sprayers — Self-propelled sprayers, pull-type sprayers, drone spraying equipment

- Tillage equipment — Discs, chisel plows, vertical tillage tools, rippers

- Grain handling and storage — Grain bins, augers, grain dryers, bucket elevators

- Irrigation systems — Center pivot systems, drip irrigation, pivots, pumping equipment

- Livestock equipment — Feedlots, feed mixers, manure handling, milking equipment

- Trucks and trailers — Grain trucks, livestock trailers, flatbeds used in farm operations

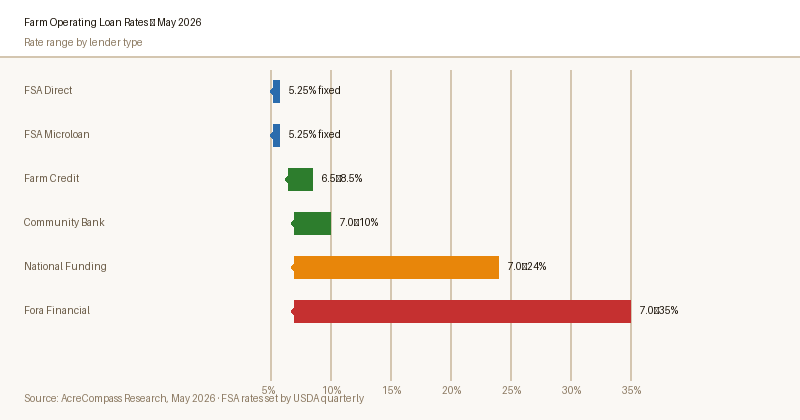

Agricultural Equipment Loan Rates — 2026

| Lender | Type | Starting Rate | Max Loan | Max Term | Min Credit | Apply |

|---|---|---|---|---|---|---|

| AgDirect | Term loan | 5.90% | $2M+ | 10 yr | 660 | Apply → |

| Farm Credit | Term / Line | 5.90%+ | $2M+ | 10 yr | 660 | Apply → |

| Southern AgCredit | Term loan | 6.25%+ | $1M+ | 7 yr | 640 | Apply → |

| Fora Financial | Term loan | 7.00%+ | $1.4M | 5 yr | 500 | Apply → |

| National Funding | Equipment loan | 7.00%+ | $500K | 5 yr | 600 | Apply → |

| Lendio | Marketplace | Varies | $5M | Varies | 550+ | Apply → |

Affiliate disclosure: AcreCompass may earn a commission through commercial lender links. Rates as of May 2026.

Equipment Loan vs. Equipment Lease: When Each Makes Sense

Choose a Loan When:

- You plan to use the equipment 500+ hours per year

- You want to build equity in the asset

- The equipment will last 10–15+ years in your operation

- You want Section 179 or bonus depreciation benefits

- You prefer a fixed monthly payment with no mileage limits

- You plan to modify or customize the equipment

Choose a Lease When:

- You need the latest technology and want to upgrade every 3–5 years

- Equipment use is seasonal or below 500 hours/year

- You want lower monthly payments than a loan offers

- Your operation is scaling and you're uncertain about long-term needs

- Off-balance-sheet treatment improves your financial ratios

- Dealer lease programs offer 0% promotional rates

Section 179 and Bonus Depreciation for Farm Equipment

The tax treatment of equipment purchases can significantly affect the economics of buying vs. leasing. Two provisions are most relevant for farm equipment buyers:

Section 179 Expensing

Section 179 allows businesses to deduct the full purchase price of qualifying equipment in the year it's placed in service, rather than depreciating it over its useful life. The 2026 Section 179 limit is $1,160,000 (adjusted annually for inflation), with a phase-out beginning at $2,890,000 in total equipment placed in service during the year.

For a farm buying a $300,000 combine, Section 179 means the full $300,000 can be deducted from taxable income in year one — creating immediate tax savings rather than spreading the deduction over 5–7 years.

Bonus Depreciation

Under current law, bonus depreciation for 2026 is 20% (the phase-down schedule reduced it from 100% in 2022 by 20 percentage points per year). This means 20% of eligible equipment costs can be deducted immediately in year one, with the remainder depreciated under normal MACRS schedules.

Section 179 is generally preferable for most farms because it provides 100% first-year deduction up to the limit, while bonus depreciation applies to a percentage of the full cost with no dollar cap.

How to Apply for Agricultural Equipment Financing

The application process for equipment financing is generally faster than for farm real estate loans because the equipment itself serves as clear, appraised collateral. Here's what most lenders require:

- Completed application with business and personal financial information

- Last 2–3 years of farm tax returns (Schedule F or business returns)

- Current farm balance sheet (assets, liabilities, net worth)

- Equipment quote or invoice from the dealer

- Description of how the equipment will be used in your operation

- Proof of existing farm insurance coverage

AgDirect and Farm Credit can often complete equipment loan approvals in 2–7 business days for established farm borrowers with complete documentation.

Fora Financial and National Funding are even faster — typically 24–48 hours — but require less documentation in exchange for higher rates.

Finance Your Next Equipment Purchase Today

Fora Financial approves agricultural equipment loans in as little as 24 hours, with financing up to $1.4 million. Or compare multiple lenders at once through Lendio's marketplace.

Frequently Asked Questions

What is the minimum credit score for farm equipment financing?

Can I finance used farm equipment?

How much down payment is required for farm equipment?

Should I finance equipment through the dealer or through my own lender?

Can I use equipment financing for a grain bin?

What happens to my equipment loan if I can't repay?

Sources

- AgDirect — Equipment Loan Rates, verified May 2026 at agdirect.com

- IRS Publication 946 — How to Depreciate Property, 2025 edition

- USDA Economic Research Service — Agricultural Resources and Environmental Indicators, 2025

- Farm Credit Administration — Annual Report on the Farm Credit System, 2025