Pros

- FSA Direct offers the lowest land loan rate in the U.S. — 4.75% fixed for up to 40 years

- FSA Down Payment program: only 5% down for qualifying beginning farmers

- Farmland appreciates over time — unlike equipment, your collateral gains value

- USDA Guaranteed loans go up to

$2.24Mwith 95% federal backing - Fixed-rate FSA loans have no prepayment penalties

Cons

- Large down payments required: 5–30% depending on program and lender

- FSA Direct requires inability to obtain credit elsewhere

- Commercial appraisals cost

$1,500–$4,000 for agricultural land - Farmland prices are at historic highs in many regions — entry costs are steep

- Property taxes, insurance, and maintenance add 1–2% annually beyond the loan payment

Who This Is For

Farmers ready to buy land for their primary operation — especially beginning farmers who can qualify for FSA Down Payment (5% down) or Direct Ownership (4.75% for 40 years). Also suited for expanding operations adding adjacent acreage.

Who Should Look Elsewhere

Farmers who need the land for less than 10 years should consider cash-rent leases instead — lower commitment and no appraisal or down payment costs. Investors buying farmland as an asset class should use commercial banks, not FSA.

Types of Farm Ownership Loans

Watch this USDA explainer video:

The farm ownership loan market is served by three distinct channels, each with different eligibility, pricing, and documentation requirements.

Understanding the differences before you start shopping will save significant time — and potentially hundreds of thousands of dollars over the life of a 30-year land loan.

- Loan-to-Value (LTV)

- The share of the land's appraised value a lender will finance. Typical farm LTV: 70-80% for cropland, 55-65% for rangeland.

- Debt Service Coverage Ratio (DSCR)

- Your net farm income divided by your total annual debt payments. Most lenders require 1.20-1.25x — meaning income must be 20-25% higher than payments.

- FSA Down Payment Program

- A beginning farmer program: you put 5% down, FSA provides 45% at a reduced rate, and a commercial bank covers the remaining 50%.

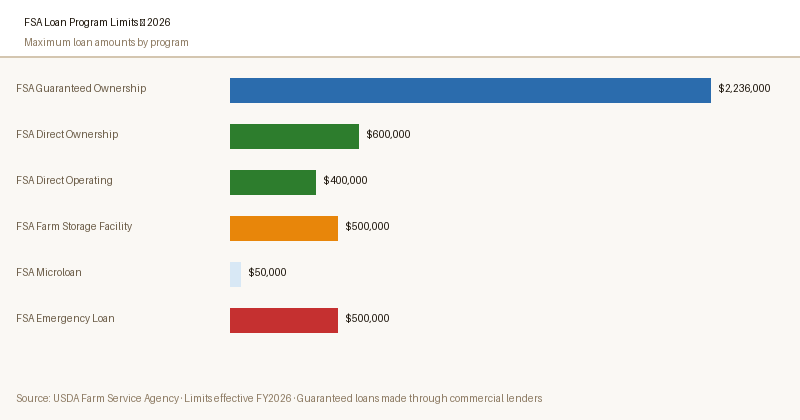

FSA Farm Ownership Direct Loans

The USDA Farm Service Agency's Farm Ownership Direct Loan program provides financing directly from the federal government to eligible farmers. Key program parameters as of May 2026:

— USDA Agricultural Data

- Maximum loan amount:

$600,000 - Interest rate: 4.75% (adjusted monthly, May 2026)

- Maximum term: 40 years

- Down payment: Typically 5% for beginning farmers; varies by applicant

- Who is eligible: U.S. citizens or permanent residents who have been operators of a family farm, are unable to obtain credit elsewhere at reasonable rates, and have a satisfactory credit history

Beginning Farmer Priority

FSA reserves a significant portion of direct ownership loan funds specifically for beginning farmers — defined as those who have been farming for 10 years or fewer and who have not been the sole owner of a farm at any point.

Beginning farmers receive priority in the application queue, making FSA particularly valuable for new agricultural operators trying to get started with land ownership.

FSA Down Payment Program

The FSA Beginning Farmer Down Payment program allows qualifying beginning farmers to purchase land with as little as 5% down. Under the program structure, FSA finances 45% of the purchase price, and a commercial lender or the seller provides the remaining 50% as a subordinate loan.

This enables beginning farmers to access land ownership with substantially less starting capital than conventional lending requires.

FSA Farm Ownership Loans — No Affiliate Relationship

AcreCompass has no affiliate relationship with USDA. Apply at fsa.usda.gov or visit your local FSA county service center. Applications for the beginning of the following year are best submitted in fall or early winter.

USDA Guaranteed Loans via Private Banks

The USDA Guaranteed Ownership Loan program allows participating banks to offer USDA-backed loans up to $2.24 million (2026 limit). The structure differs fundamentally from the direct program: you borrow from your bank, and USDA guarantees up to 95% of the loan.

If you default, USDA pays the bank — reducing the bank's risk enough that they can offer better rates than they'd provide unguaranteed.

Guaranteed loans are faster than direct loans — typically 2–4 weeks versus 30–60 days — because the bank handles underwriting while USDA simply reviews and approves the guarantee.

For farmers with adequate credit history who simply need a larger loan than the $600K direct limit, the guaranteed program is the logical next step.

Farm Credit Services

Farm Credit is a network of member-owned agricultural lending cooperatives — the largest private source of agricultural credit in the United States.

Unlike banks, Farm Credit exists specifically to serve agricultural borrowers, meaning their products, appraisal standards, and lending criteria are calibrated to farming realities rather than commercial banking risk frameworks.

Farm Credit's 30-year fixed rate farm mortgages start at approximately 5.85% as of May 2026 — competitive with or lower than most commercial banks for qualified borrowers.

The cooperative structure means that a portion of Farm Credit earnings are returned to borrowers as patronage dividend (a rebate Farm Credit associations pay back to borrower-members from annual profits)s, which effectively reduces the net interest cost by 0.25–0.75% depending on the cooperative's performance.

Southern AgCredit, Farm Credit Services of America, Farm Credit Mid-America, and other regional associations operate under the Farm Credit umbrella and serve different geographic regions.

Contact the Farm Credit association serving your county to begin an application.

Commercial Bank Farm Mortgages

Commercial banks — from major agricultural lenders like Farm Bureau Bank to local community banks with agricultural portfolios — offer farm real estate loans outside of FSA and Farm Credit channels. Commercial bank farm mortgages typically require:

- Down payment: 20–25% is standard; some banks accept 10–15% with mortgage insurance

- Loan-to-value: 70–80% of appraised land value

- Credit score: 680+ preferred; 700+ for best rates

- Debt service coverage: Typically 1.20–1.25x (farm income must cover loan payments with margin)

- Terms: 15–25 years common; some banks offer 30-year terms for well-qualified borrowers

Down Payments and LTV in Agricultural Lending

Agricultural land appraisals differ from residential appraisals in that farmland is valued primarily on income-producing potential — comparable sales, productivity index, and capitalized rental income — rather than improvements. Lenders typically lend against the lower of appraised value or purchase price.

Typical loan-to-value ratios by lender type:

- FSA Direct: Up to 95% for beginning farmers (5% down); typically 85–90% for other applicants

- USDA Guaranteed: Up to 95% of appraised value

- Farm Credit: Typically 65–80% LTV; varies by land type and borrower profile

- Commercial Banks: 65–80% LTV; requires 20–35% down

Farm Ownership Loan Comparison Table

| Program | Max Loan | Rate | Max Term | Min Down | Apply |

|---|---|---|---|---|---|

| FSA Direct Ownership | $600K | 4.75% | 40 yr | 5% | Visit FSA → |

| FSA Guaranteed | $2.24M | Bank rate + USDA | 40 yr | 5–10% | Visit FSA → |

| Farm Credit Services | $2M+ | 5.85%+ | 30 yr | 15–20% | Apply → |

| Southern AgCredit | $1M+ | 6.00%+ | 30 yr | 20% | Apply → |

| Lendio (Bank Marketplace) | $5M | Varies | 25 yr | 20–25% | Apply → |

Affiliate disclosure: Commercial lender links may earn AcreCompass a commission. FSA links are not affiliate links. Rates as of May 2026.

Ready to Finance Your Farm Purchase?

Southern AgCredit specializes in farm real estate in the southeastern United States with competitive 30-year rates. Or use Lendio to compare multiple bank offers with a single application.

Frequently Asked Questions

What is the FSA Farm Ownership loan rate in 2026?

How much down payment do I need to buy a farm?

How long can a farm ownership loan be?

Can I get a farm ownership loan for land I already have under contract?

What is the difference between a direct and guaranteed FSA ownership loan?

Do farm lenders require an appraisal when buying farmland?

$1,500–$4,000 depending on farm size and complexity, and take 2–4 weeks to complete.Can I use a farm ownership loan to buy land and build a farm structure?

Sources

- USDA Farm Service Agency — Farm Ownership Loan Programs, rates verified May 2026

- USDA Farm Service Agency — Farm Loan Program Annual Activity Report, Fiscal Year 2025

- Farm Credit Administration — 2025 Annual Report

- USDA Economic Research Service — Farm Real Estate Values and Rental Rates, 2025