Who This Is For

Grain farmers navigating the 60–120 day cash flow gap between harvest expenses and grain sale revenue. Especially useful for operations considering storage strategies to capture basis improvement over winter months.

Who Should Look Elsewhere

Livestock operations and farms that sell production at harvest (no storage strategy) face different cash flow timing — focus on operating line renewal instead.

The Harvest Cash Flow Gap

For grain farmers — corn, soybeans, wheat, sorghum — the cash flow calendar creates a predictable problem every year. Harvest costs spike in September–October.

Grain is sold in waves from October through February, depending on storage capacity, price strategy, and basis levels. Meanwhile, rent payments, land notes, operating loan repayments, and fall input purchases come due on their own schedule.

The result is a 60–120 day gap between when you incur expenses and when grain revenue arrives. For a 1,000-acre corn operation with $600,000 in annual operating costs, bridging a 90-day gap can require $100,000–$200,000 in short-term financing.

Typical Grain Farm Cash Flow Cycle

Costs peak

Watching basis

No revenue yet

Payment arrives

USDA Marketing Assistance Loans (MAL)

The USDA Commodity Credit Corporation (CCC) Marketing Assistance Loan program is arguably the most underused financing tool in grain farming. Here's how it works:

- You store grain in an approved on-farm or commercial storage facility after harvest.

- You use that stored grain as collateral to borrow from USDA at the county loan rate.

- Loan rates for corn are typically around

$1.98–$2.20/bushel depending on county; soybeans $5.00–$5.50/bushel. These translate to approximate annual interest rates of ~1.25%. - The loan term is 9 months maximum (CCC loan).

- When you sell the grain, you repay the loan plus accrued interest. If commodity prices rise above the loan rate, you keep the difference.

MAL loans are available at your county FSA office with no credit check beyond standard FSA eligibility. They can fund within days of application if your storage is certified and the grain is in place.

No disaster declaration, hardship application, or special eligibility beyond being a grain-producing farm operation is required.

LDP (Loan Deficiency Payment) Alternative

If the county price falls below the loan rate on a given day, you can take an LDP instead of an MAL — a direct payment equal to the difference per bushel.

LDPs and MALs are mutually exclusive for the same bushels. Your county FSA office can show you current county prices versus loan rates to determine which is advantageous.

Farm Operating Lines of Credit

A seasonal operating line of credit — drawn down at planting and repaid after grain sale — is the most common bridge tool for established grain operations.

The revolving nature is key: you can draw what you need when bills come due, pay it back when checks arrive, and interest accrues only on the outstanding balance.

For existing Farm Credit or community bank relationships, fall operating line renewals are routine. Most lenders will size your line at 70–80% of projected gross crop revenue, adjusted for crop insurance coverage. A 1,000-acre corn operation projecting

— USDA Agricultural Data$600/acre gross revenue might qualify for a $360,000–$480,000 operating line.

The bridge strategy: draw down your line in October to cover harvest costs and fall bills, then repay from grain sale proceeds in December–February.

If you're holding grain for spring prices, your line may need to carry the balance longer — make sure your lender knows your grain marketing plan and is comfortable with the extended carry.

Grain Storage Loans

Separate from operating loans, USDA and some commercial lenders offer financing specifically for building or leasing additional grain storage.

Holding grain through winter to capture spring basis improvement requires storage capacity, and storage financing can pay for itself quickly if the basis move covers the interest cost.

USDA's Farm Storage Facility Loan (FSFL) offers rates at or below commercial rates for on-farm grain storage construction. Maximum loan is $500,000, terms up to 12 years.

Applications go through your county FSA office. Commercial storage construction loans are available through Farm Credit institutions and most agricultural community banks.

$12,500. Storage financing cost at 7% on $200,000 for 6 months = $7,000. Net gain: $5,500 — if basis performs as expected.Commercial Bridge Options

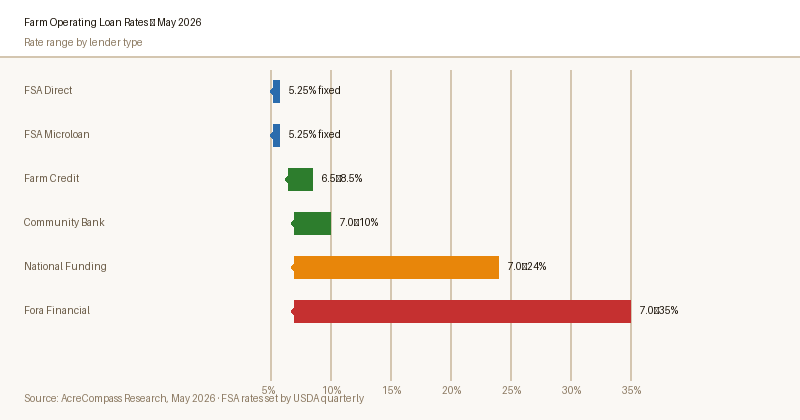

For situations where MAL doesn't apply (livestock operations, specialty crops without a USDA loan rate), or when your operating line is fully drawn, commercial lenders offer short-term bridge financing:

| Lender | APR (annual percentage rate) Range | Max Amount | Funding Speed |

|---|---|---|---|

| National Funding | 7–24% | $500,000 | 24 hours |

| Fora Financial | 7–35% | $1.4M | 24–48 hours |

| Lendio | Varies | $5M | 2–7 days |

Commercial bridge loans make sense when the alternative is a forced grain sale at harvest lows. If selling corn in October at $4.50/bushel vs.

January at $5.00/bushel, the 50-cent/bushel improvement on 40,000 bushels = $20,000. A 90-day bridge loan at 18% APR on $150,000 = $6,750 in interest. Net improvement: $13,250 — if prices perform.

Crop Insurance and Cash Flow

If you experience a crop loss, crop insurance indemnity payments can help bridge harvest cash flow — but the timing is important to understand before you budget against it.

The typical timeline after a loss is confirmed: file a Notice of Loss within 72 hours of discovering damage. Adjuster visit: 5–15 business days.

Loss determination and claim filing: another 7–14 days after adjuster visit. Payment processing: 30 days after claim approval. Total realistic timeline from loss to check: 45–75 days.

This means crop insurance indemnity should not be counted on for October or November cash flow needs — it will more likely arrive in December or January.

Plan your bridge financing accordingly, and use your operating line or MAL loan to cover the gap while the claim processes.

Creating a Harvest Cash Flow Budget

A simple harvest cash flow budget helps you size your bridge financing need accurately. For each month from September through February, list:

- Cash outflows: Harvest costs (fuel, custom hire, repairs), fall rent payments, operating loan repayment deadlines, fall fertilizer pre-pays, family living draw

- Cash inflows: Grain sales (by month based on your marketing plan), crop insurance payment (estimated arrival), FSP/ARC payments (typically December–January)

- Monthly net: Outflows minus inflows

- Cumulative shortfall: Running total of the deficit — this is your bridge financing need

Most grain operations find their peak bridge financing need occurs in November, before significant grain sales and after harvest costs have hit.

Sizing your MAL or operating line draw to cover that peak deficit — not the full season's expenses — minimizes interest cost.

Bridge Your Harvest Cash Flow Gap

Compare your options: USDA MAL loans at ~1.25% through your county FSA office, or commercial bridge financing from National Funding for same-day decisions.