Who This Is For

Farmers who need operating capital for spring planting — especially those applying for FSA loans, renewing Farm Credit lines, or considering commercial bridge financing. Start planning in December–January for an April–May planting window.

Who Should Look Elsewhere

Farmers with fully funded operating lines or sufficient cash reserves for input purchases. If your line is already confirmed and drawn, this guide's timeline does not apply to you.

The Spring Planting Loan Timeline

Spring planting creates one of the most time-compressed financing needs in agriculture. Corn planting windows in the Corn Belt run roughly April 20 through May 15 — a 25-day window that determines your entire season.

You need seeds, fertilizer, and fuel purchased before that window opens, which means financing needs to be in place by late March at the latest.

Working backward from a late-March funding target: most banks require 2–4 weeks for underwriting. FSA direct loans require 4–8 weeks. That means the practical application window for FSA is December through February for spring planting purposes.

Banks and Farm Credit institutions have more flexibility but reward early applications with faster processing when their underwriters aren't flooded.

The other timing factor is FSA loan authority. USDA allocates operating loan authority by county at the start of each federal fiscal year (October 1).

Popular counties — especially in the Corn Belt — can exhaust that authority by February or March, meaning even complete applications get waitlisted. Calling your county service center in January to check remaining authority is well worth 10 minutes.

Three Ways to Finance Spring Inputs

1. FSA Direct Operating Loan

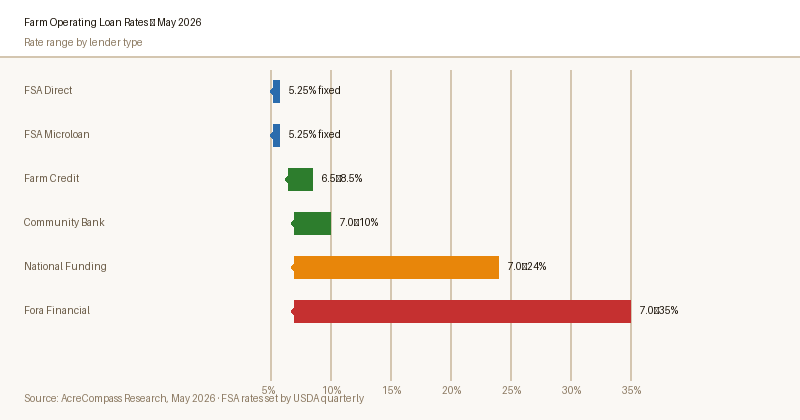

The USDA Farm Service Agency offers direct operating loans at 5.25% (as of May 2026) — the lowest rate available outside of specific state programs. Maximum loan size is

— USDA Agricultural Data$400,000. The catch: you must be unable to obtain credit elsewhere, the application process takes 4–8 weeks, and loan authority is finite by county.

Who it's best for: beginning farmers, operators with recent credit challenges, or those who have been turned down by commercial lenders. If you have clean credit and an established Farm Credit relationship, FSA direct is probably not your fastest path.

2. Farm Credit Operating Line of Credit

Farm Credit institutions (FCS, AgriBank, CoBank, etc.) offer seasonal operating lines of credit tailored to agricultural cash flow cycles.

You draw down at planting and repay after harvest — interest accrues only on the outstanding balance. Rates typically run 6.5–8.5% depending on credit profile and institution.

Renewal of an existing line is fast — often 3–7 days if your financial statements are in order. A new Farm Credit relationship takes longer: plan on 3–6 weeks and have 2–3 years of Schedule F returns, a farm balance sheet, and a crop budget ready.

3. Commercial Lender (National Funding, Fora Financial, Lendio)

For farmers who need funding quickly — especially in February or March when other options are closing — commercial lenders offer operating capital at higher rates but with same-day to 3-day funding timelines.

National Funding has funded agricultural operating loans in as little as 24 hours.

The tradeoff is cost: commercial rates run 7–35% APR (annual percentage rate), which on a $200,000 operating loan adds $14,000–$70,000 in annual interest vs. $10,500 at FSA rates.

Use these lenders as a bridge when the alternative is missing your planting window, not as a first choice.

Current Spring Operating Loan Rates (May 2026)

| Lender | APR Range | Max Amount | Funding Speed | Best For |

|---|---|---|---|---|

| FSA Direct | 5.25% | $400,000 | 4–8 weeks | Best rate; beginning farmers |

| Farm Credit | 6.5–8.5% | $5M+ | 1–3 weeks | Existing relationships; large ops |

| National Funding | 7–24% | $500,000 | 24 hours | Fast bridge; late March rush |

| Fora Financial | 7–35% | $1.4M | 24–48 hours | Larger fast-funding needs |

| Lendio | Varies | $5M | 2–7 days | Compare multiple offers at once |

Rates as of May 2026. APR ranges reflect variation by borrower credit profile. Always get a written rate quote before committing.

Spring Planting Loan Checklist: By Month

-

January

Start FSA Application / Confirm Farm Credit Renewal

Call your county FSA service center to check remaining loan authority. Book an appointment. If you have a Farm Credit relationship, initiate renewal paperwork now — don't wait for your AO to call you.

-

February

Gather Documents / Submit Application

Compile 3 years of Schedule F returns, current farm balance sheet, crop budget for the coming year, proof of crop insurance, and any lease agreements for rented ground. Submit FSA application by mid-February for spring planting use.

-

Early March

Target Approval

Follow up with your lender on underwriting status. If FSA is running long, get a commercial pre-approval as a backup — you can decline it if FSA comes through in time.

-

Late March

Drawdown Funds / Purchase Inputs

With approval in hand, draw down your operating line and purchase seeds, fertilizer, and fuel ahead of your planting window. Pre-buying inputs often secures better pricing than buying at planting time.

If It's Already March: Fast Options

If you're reading this in March or April and haven't secured operating financing yet, here's your realistic playbook:

- Check your existing Farm Credit line first. If you have any existing relationship, call your ag loan officer today. Renewal can happen in days if your financials are current.

- National Funding — 24-hour funding. Apply online, get a decision same day, fund within 24 hours. Rates are higher, but missing planting is worse. Use their calculator to see your monthly cost before committing.

- Lendio marketplace. One application compared across 75+ lenders. Good if you're uncertain about your credit profile — see actual offers before picking.

- Input financing direct from suppliers. Major seed and fertilizer dealers offer financing at 0% for 90 days (occasionally), which can bridge you to a longer-term solution.

$150,000 operating loan costs $2,250/month in interest. If you pay it off after your October harvest — 6 months — total interest cost is $13,500. Compare this to the revenue impact of a delayed or missed planting window before deciding.What Spring Operating Loans Can Cover

FSA operating loans and most commercial operating loans can fund:

- Seed (corn, soybeans, wheat, specialty crops)

- Fertilizer and soil amendments (nitrogen, phosphorus, potassium)

- Pesticides, herbicides, and fungicides

- Fuel (diesel, propane) for planting equipment

- Crop insurance premiums (spring policies)

- Hired labor for planting operations

- Custom application services

- Small equipment purchases (generally up to

$30,000under operating loan rules)

Operating loans cannot be used to purchase land or fund major equipment purchases — those require separate financing. FSA operating loans also cannot fund living expenses, though some commercial lines are more flexible on use restrictions.

Need Operating Financing Fast?

Compare your options before planting season — get a rate from National Funding in minutes, or check FSA operating loan availability at your county service center.