Who This Is For

Farmers deciding between applying directly to FSA (lower rate, more paperwork, smaller limit) or going through a commercial bank with FSA backing (faster, larger limit, negotiated rate). Read this comparison before applying to either.

Who Should Look Elsewhere

Farmers who already know they want commercial speed and can afford market rates should skip FSA entirely and apply to Farm Credit or an online lender. Farmers who only need equipment financing should look at AgDirect instead.

Understanding the Two Pathways

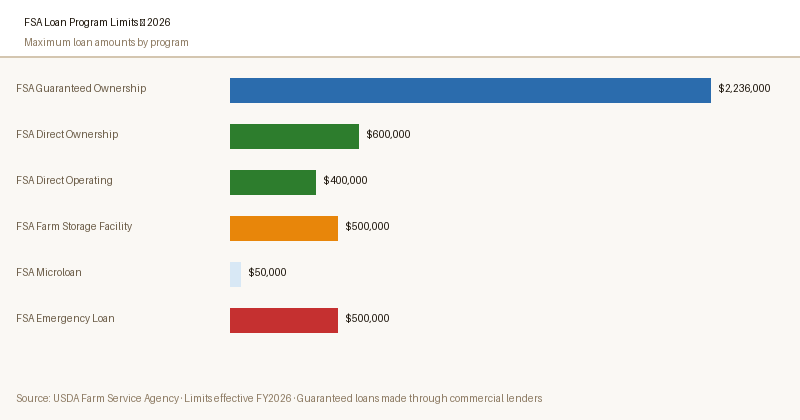

$600K; Guaranteed loans reach $2.24M through commercial lenders.Watch this USDA explainer video:

Every year, thousands of farmers face the same question: which FSA loan pathway should I pursue?

The answer depends on four factors: how much you need to borrow, your current credit profile, how quickly you need the funds, and whether you have an existing banking relationship.

- Direct Loan

- USDA lends directly to the farmer at government-set rates. Requires the credit-elsewhere test. Maximum

$600,000ownership / $400,000 operating. - Guaranteed Loan

- A commercial bank makes the loan; USDA guarantees 95% of it against default. No credit-elsewhere test. Maximum

$2,236,000. - Down Payment Program

- A beginning farmer program where FSA provides 45% of the purchase price and the buyer puts 5% down, with a commercial lender funding the remaining 50%.

Direct loans are loans from USDA itself — the federal government is literally your lender. Guaranteed loans are commercial loans where your bank takes the risk but USDA promises to cover up to 95% of the lender's loss if you default. From a borrower's perspective, the paperwork differs substantially, and the rate structures are very different.

— USDA Farm Service Agency — Loan Program Overview

Full Side-by-Side Comparison

| Feature | FSA Direct Loan | FSA Guaranteed Loan |

|---|---|---|

| Who lends the money | USDA directly | Private bank or lender |

| Max loan — Ownership | $600,000 | $2,236,000 |

| Max loan — Operating | $400,000 | $2,236,000 |

| Interest rate | Set by USDA quarterly (5.50% ownership, 5.25% operating — May 2026) | Negotiated with lender (typically 6–8% in current market) |

| "Can't get credit elsewhere" required | Yes — must demonstrate inability to get commercial credit | No — open to creditworthy borrowers |

| Typical approval time | 30–60 days | 2–4 weeks |

| Beginning farmer priority | Yes — dedicated set-asides | Yes — dedicated set-asides |

| Where you apply | Your local county FSA service center | A participating commercial lender |

| USDA guarantee | N/A (USDA is the lender) | 95% of loan amount |

| Rate type | Fixed for life of loan | Fixed or variable (lender's choice) |

| Prepayment penalty | None | None required by FSA; lender terms vary |

| Loan term — Ownership | Up to 40 years | Up to 40 years |

| Loan term — Operating | Up to 7 years | Up to 7 years |

When to Choose a Direct Loan

A Direct loan is typically the right choice when you meet the "unable to obtain credit elsewhere" standard and one or more of the following applies:

Choose FSA Direct When...

- Commercial lenders have declined your application or offered rates you can't service

- You are a first-time or beginning farmer with limited credit history

- Your loan amount is within the Direct limits ($600K ownership, $400K operating)

- You want the absolute lowest fixed rate available for farm financing

- You don't have an established commercial banking relationship

- Your credit profile needs rebuilding — FSA Direct is often a stepping stone to commercial credit

A critical note: qualifying for a Direct loan doesn't mean you're a risky borrower.

FSA's mission is to serve farmers who are underserved by commercial credit markets — that includes beginning farmers, operators of small farms, and farmers in rural communities with limited lending options.

When to Choose a Guaranteed Loan

Choose FSA Guaranteed When...

- You need more than $600,000 (Guaranteed allows up to

$2.24M) - You have an established relationship with a local bank that participates in FSA programs

- You need faster processing — 2–4 weeks vs. 30–60 days for Direct

- You do not meet the "can't get credit elsewhere" requirement for Direct

- Your commercial bank's rate with the USDA guarantee is competitive with the Direct rate

- You prefer to work with a local lender who knows your farm and region

How to Apply for Each

Applying for a Direct Loan

Direct loan applications go through your local county FSA service center. Schedule a pre-application meeting with your loan officer — this free consultation is the best way to understand what documents you need and whether you're likely to qualify.

The meeting also starts the clock on FSA's "unable to obtain credit" determination.

You'll complete FSA Form 2001 (Farm Loan Application) and submit supporting documentation including 3 years of tax returns, a balance sheet, and a cash flow projection. The county loan officer reviews your file and forwards it for final approval.

Applying for a Guaranteed Loan

For a Guaranteed loan, you work directly with your participating commercial lender — not with FSA.

Your bank assesses your creditworthiness, structures the loan, and submits a guarantee request to FSA on your behalf. The bank needs FSA's conditional approval before closing.

This process typically takes 2–4 weeks from complete application to closing. The bank does most of the work; your role is to provide financial documentation and work with your lender's underwriting team.

Ready to Start Your FSA Loan Application?

For a Direct loan: find your county FSA office. For a Guaranteed loan: ask your bank if they participate in FSA programs, or find a participating lender at fsa.usda.gov.

Visit USDA FSA →AcreCompass has no affiliate relationship with USDA.

Frequently Asked Questions

Can I apply for both a Direct and a Guaranteed loan at the same time?

Is the interest rate on a Guaranteed loan always higher than a Direct loan?

How long do I have to use a Direct loan before I'm expected to refinance with a commercial lender?

What happens if my Guaranteed lender goes out of business?

Do Guaranteed loans require the same documentation as Direct loans?

Are Guaranteed loan rates fixed or variable?

What is the FSA Down Payment Loan Program?

Sources

- USDA FSA — Farm Loan Programs

- USDA FSA — Direct and Guaranteed Loan Regulations (7 CFR Parts 764, 762)

- USDA Economic Research Service — Farm Financial Conditions, 2025