Pros

- USDA subsidizes 38–70% of your premium — the federal government pays the majority of the cost

- Covers 100+ crops with coverage levels from 50% to 85%

- 490 million acres covered in 2024 — the backbone of U.S. agricultural risk management

- Revenue Protection policies cover both price drops and yield losses simultaneously

- No credit check or financial qualification required — any farmer can buy it

Cons

- Sales closing deadlines are strict — miss the date and you cannot buy coverage that crop year

- Must be purchased through a private crop insurance agent (not available online)

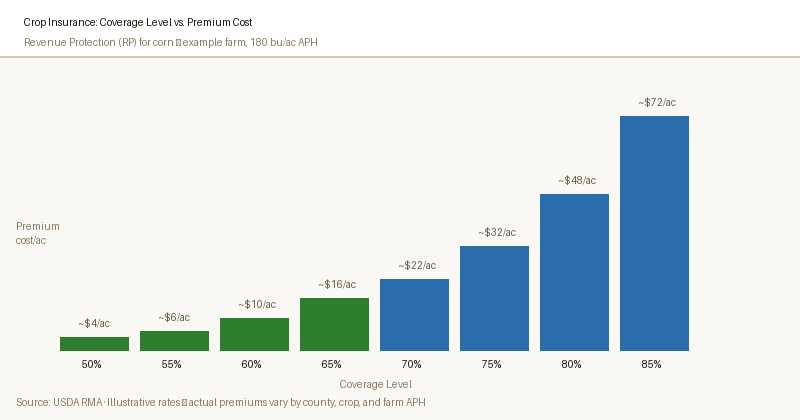

- Higher coverage levels (80–85%) are expensive even with subsidies

- Claim payouts take 45–75 days — not instant cash after a loss

- APH-based coverage can be reduced by years of poor yields, creating a downward spiral

Who This Is For

Every farmer growing insurable crops. Federal crop insurance is the foundation of agricultural risk management — most lenders require it as a condition of financing, and the USDA subsidy makes it the cheapest catastrophic protection available.

— USDA Risk Management Agency

Who Should Look Elsewhere

Highly diversified farms growing 3+ commodities may get better value from WFRP (Whole-Farm Revenue Protection) than from individual crop policies. Livestock-only operations should look at LRP and LGM policies instead.

The Two Main Types of Crop Insurance

Watch this USDA explainer video:

The federal crop insurance program offers dozens of policy types, but the vast majority of acres are insured under two basic structures: Yield Protection and Revenue Protection.

- Revenue Protection (RP)

- Crop insurance that pays when your per-acre revenue (yield x price) falls below your guarantee. Uses the higher of projected or harvest price.

- Yield Protection (YP)

- Crop insurance that pays only when your actual yield falls below your APH guarantee. Does not respond to price changes.

- Actual Production History (APH)

- Your farm's 4-to-10-year yield average, used as the basis for your crop insurance guarantee. Higher APH = higher coverage.

- Sales Closing Date

- The deadline by which you must purchase or change your crop insurance policy for a given crop year. Missing it means no coverage.

| Feature | Yield Protection (YP) | Revenue Protection (RP) |

|---|---|---|

| What it covers | Yield loss below your APH guarantee | Revenue loss due to yield shortfall OR price decline |

| Price used for indemnity | Projected price at planting time | Higher of projected price or harvest price |

| Premium cost | Lower | Higher |

| Market share | ~20% of corn/soybean policies | ~65% of corn/soybean policies |

| Best for | When commodity prices are stable | Most situations, especially volatile price years |

Revenue Protection also has a variant: RP with Harvest Price Exclusion (RP-HPE). This version uses only the projected price for indemnity calculations (like YP) but still covers revenue shortfalls from yield loss.

It costs less than full RP and more than YP — a middle-ground option. See our RP vs. YP comparison guide for a full breakdown.

How Premiums Are Calculated

Your crop insurance premium is set by RMA (Risk Management Agency)'s actuarial tables and based on four factors:

- Coverage level — from 50% to 85% of your APH yield guarantee (higher coverage = higher premium)

- Actuarial rate — RMA's calculated loss rate for your crop type and county

- Your APH — your farm's actual production history average (higher APH = higher dollar liability)

- Number of acres insured

USDA subsidizes a portion of this premium. The exact subsidy depends on your coverage level:

| Coverage Level | Your Share of Premium | USDA Share |

|---|---|---|

| 50% | 35% | 65% |

| 55% | 32% | 68% |

| 60% | 32% | 68% |

| 65% | 30% | 70% |

| 70% | 30% | 70% |

| 75% | 45% | 55% |

| 80% | 48% | 52% |

| 85% | 62% | 38% |

Note: Subsidy rates apply to most basic policies. Enterprise Unit and Basic Unit policies receive higher subsidy rates. Optional Unit policies receive lower subsidies. Consult your agent for your specific policy's subsidy level.

How to Buy Crop Insurance

Crop insurance is sold exclusively through USDA-approved private insurance agents. You cannot buy a policy directly from USDA or RMA. The agent works with you to select the right policy type, coverage level, and unit structure for your operation.

Steps to purchase crop insurance:

- Find an approved agent using the RMA agent locator at rma.usda.gov — search by state and crop

- Meet with the agent to review your APH records and choose a policy type and coverage level

- Sign and submit your application before your crop's sales closing date

- Pay your premium (or arrange premium financing) — due before or at planting in most cases

Sales Closing Dates

Sales closing dates are set by RMA and vary by crop and county. Miss the closing date and you cannot purchase coverage for that crop year. Most major crops have closing dates weeks or months before planting begins.

| Crop | Corn Belt States | Southern Plains | Southeast |

|---|---|---|---|

| Corn | March 15 | March 15 | Varies by county |

| Soybeans | March 15 | March 15 | Varies by county |

| Winter Wheat | September 30 | August 31 – Sept 30 | October 31 |

| Cotton | N/A | March 15 | March 15 |

| Grain Sorghum | March 15 | March 15 | Varies by county |

| Peanuts | N/A | March 15 | March 15 |

Sales closing dates are set by RMA and may change annually. Always verify your exact deadline at rma.usda.gov or with your agent.

How to File a Claim

If your crop experiences a loss, you must notify your insurance agent within 72 hours of discovering the damage (or within 15 days of final harvest for yield-based losses). Failing to provide timely notice of loss can result in denial of your claim.

The claims process works as follows:

- Notify your agent immediately upon discovering loss — do not destroy evidence or harvest the damaged area before the adjuster visits

- An approved crop insurance adjuster visits your farm to assess the loss and measure damaged areas

- Your final yield is determined by the adjuster (for yield-based claims) or by comparing harvest records to your APH guarantee

- If an indemnity is owed, payment is typically issued within 30 days of final claim determination

What Is Actual Production History (APH)?

Your Actual Production History is the average of your farm's yield records over the last 4–10 years, used to set your yield guarantee.

If your APH for corn is 180 bu/ac and you purchase 80% coverage, your guarantee is 144 bu/ac (180 × 80%). A loss occurs when your actual harvest falls below 144 bu/ac.

APH records are maintained by your insurance agent and must be verified with yield documentation (such as scale tickets or settlement sheets).

Low-yield years from disasters can sometimes be excluded from the APH calculation under RMA rules. See our APH explainer article for full details on how to manage your yield history.

Find Your Crop Insurance Agent

Crop insurance must be purchased through a USDA-approved agent — search by state and crop type at the RMA website. AcreCompass does not sell insurance.

Find an Agent at RMA →AcreCompass does not sell crop insurance and earns no commission on policy purchases.

Frequently Asked Questions

Is crop insurance required to get an FSA (Farm Service Agency) loan?

Can I switch from YP to RP mid-season?

What happens if a hailstorm destroys part of my field but not all of it?

What is a deductible in crop insurance?

How does crop insurance interact with ARC-CO and PLC farm bill programs?

Do I need crop insurance if I have strong financial reserves?

$15,000–$25,000 of your annual premium. Declining crop insurance means declining that subsidy. Most ag lenders also require coverage regardless of the borrower's financial strength.Can I insure an organic crop?

What is Whole-Farm Revenue Protection (WFRP)?

Sources

- USDA Risk Management Agency — Crop Insurance Program

- USDA RMA — Summary of Business Reports, 2024 Crop Year

- USDA Economic Research Service — Federal Crop Insurance: Background, Costs, and Selected Topics, 2025

- USDA RMA — Premium Subsidy Tables, Policy Year 2026