Pros

- Rate of approximately 2.50% (CCC rate) — the lowest fixed-asset financing available to farmers

- No credit-elsewhere test required — simpler qualification than other FSA (Farm Service Agency) programs

- The facility itself serves as collateral — no additional real estate lien

- Saves

$30K–$50K vs. commercial financing on a $200K structure over 10 years - 12-year terms for permanent structures provide manageable monthly payments

Cons

- 15% down payment required —

$30Kon a $200K grain bin - On-farm structures only — rented or off-site storage does not qualify

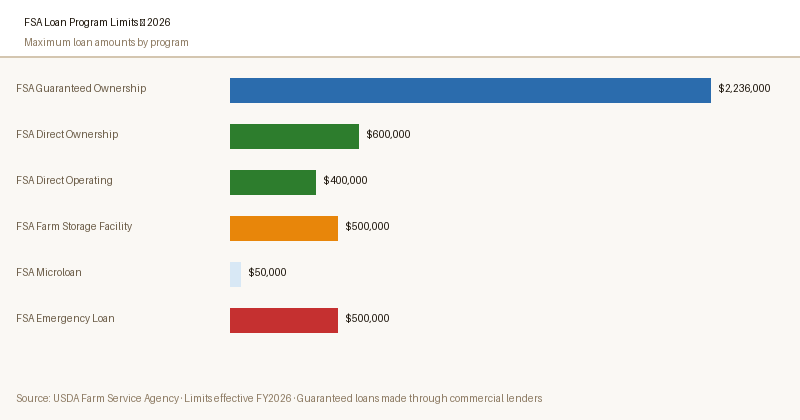

- Maximum $500K per borrower caps the program for large operations

- Minimum loan is $50K — not suitable for small portable storage

- Approval takes 3–4 weeks even though the application is simpler than other FSA programs

Who This Is For

Grain, hay, and specialty crop farmers who want to store production on-farm to market at higher prices. Ideal for operations building grain bins, cold storage, or hay barns that cost $50K–$500K.

— USDA Farm Service Agency — Farm Storage Facility Loan Program

Who Should Look Elsewhere

Farmers who already have adequate storage or sell at harvest should not take on storage facility debt. Operations needing more than $500K in storage should combine FSFL with commercial financing.

What Is the FSFL Program?

$50,000.The Farm Storage Facility Loan program is administered by the USDA Farm Service Agency and designed to help producers store eligible commodities on their farms.

By storing grain on-site rather than in commercial elevators, farmers gain more flexibility to market their crops when prices are favorable — rather than selling at harvest when prices may be depressed.

The FSFL stands apart from other FSA loan programs in two important ways: it carries the lowest interest rate of any USDA farm loan (tied to the CCC borrowing rate), and it does not require you to demonstrate that you can't obtain credit elsewhere.

If you produce an eligible commodity and have a farm where storage will be built, you're broadly eligible.

What You Can Finance

FSFL covers a wide range of on-farm storage infrastructure. Eligible facilities and equipment include:

- Grain bins and silos (hopper-bottom and flat-bottom)

- Flat storage buildings (hay, grain, commodity sheds)

- Refrigerated storage and cold storage facilities

- Handling equipment that is permanently affixed to eligible storage facilities (bucket elevators, conveyors, aeration systems)

- Grain drying equipment connected to eligible storage

- Portable storage structures (with specific requirements)

What You Cannot Finance

✓ Eligible

- Grain bins (on-farm)

- Cold storage facilities

- Hay sheds

- Peanut storage

- Aeration and drying systems

- Permanently attached handling equipment

- Portable storage (qualifying types)

✗ Not Eligible

- Processing or milling equipment

- Transportation or hauling equipment

- Commercial off-farm storage

- Storage for non-eligible commodities

- Facility repairs (new construction only)

- Land purchase

- Working capital or operating expenses

Eligible Commodities

To qualify for the FSFL, you must produce a commodity that is eligible for CCC price support programs or be an eligible commodity as defined by the Farm Bill. Major eligible commodities include:

| Commodity Category | Examples |

|---|---|

| Row Crops | Corn, soybeans, grain sorghum, wheat, barley, oats, rye, canola |

| Cotton & Oilseeds | Upland cotton, extra-long staple cotton, sunflower, flaxseed, safflower, sesame |

| Legumes | Peanuts, dry peas, lentils, small chickpeas, large chickpeas |

| Forage | Hay, silage |

| Specialty Crops | Eligible sugar crops, tobacco (with restrictions), rice |

| Fresh Produce (cold storage) | Fruits and vegetables (requires refrigerated facility loan type) |

FSFL Interest Rates

The FSFL rate is tied to the CCC borrowing rate, which is set by the U.S. Treasury. Unlike other FSA loan rates that update quarterly, the CCC rate updates more frequently based on Treasury borrowing costs.

In April 2026, the rate stands at approximately 2.50% — making FSFL one of the lowest-cost financing options available for any farm improvement.

The rate is fixed at loan closing for the life of the FSFL — you lock in the rate you receive when you close on your loan, regardless of future CCC rate changes. This makes FSFL loans highly attractive in periods when the CCC rate is low.

$200,000 grain bin financed over 10 years, this rate difference can save $30,000–$50,000 in interest.Loan Limits and Terms

| Parameter | Details |

|---|---|

| Minimum loan amount | $50,000 |

| Maximum loan amount | $500,000 per borrower |

| Down payment required | 15% of total project cost |

| Maximum term — permanent structures | 12 years |

| Maximum term — portable structures | 7 years |

| Maximum term — handling equipment only | 7 years |

| Collateral | The storage facility itself serves as collateral |

| Location requirement | Storage must be located on the farm where the commodity is produced |

How to Apply

FSFL applications are processed at your local county FSA service center — the same office where you'd apply for other FSA loans.

The process is generally simpler than a Direct farm ownership or operating loan because the "unable to obtain credit elsewhere" requirement does not apply.

Basic requirements for application:

- Proof that you produce an eligible commodity

- Construction quotes or bids for the proposed facility

- Evidence of farm ownership or long-term lease of the property where storage will be located

- Evidence that the 15% down payment is available

- Basic financial information (current balance sheet)

You do not need 3 years of tax returns or a detailed cash flow projection for most FSFL applications, making this a faster and simpler process than other FSA loan types.

Contact your county FSA office to start the process and confirm current documentation requirements.

Is the FSFL Right for You?

Compare FSFL to the two most common alternatives for financing on-farm storage:

| Feature | USDA FSFL | Commercial Equipment Loan | Grain Storage Lease |

|---|---|---|---|

| Typical rate | ~2.50% | 6–9% | N/A (lease payments) |

| Down payment | 15% required | 10–20% typical | None or first/last month |

| Own the facility | Yes — you own it | Yes — you own it | No |

| Approval time | 3–4 weeks | 1–3 weeks | Immediate |

| Max loan / commitment | $500,000 | Lender-dependent | Ongoing obligation |

| Best for | Long-term storage investment at lowest cost | When speed matters or FSFL limit is reached | When you need temporary or seasonal storage only |

For most grain and commodity farmers who plan to store on-farm for multiple years, the FSFL is the clear winner on cost. The 15% down payment and application process are modest hurdles compared to the lifetime interest savings.

Apply for an FSFL at Your County FSA Office

The application process is simpler than other FSA loan types and doesn't require proving inability to get credit elsewhere.

Visit USDA FSA →AcreCompass has no affiliate relationship with USDA.

Frequently Asked Questions

Can I use the FSFL to upgrade an existing grain bin?

Is the $500,000 limit per structure or per farm operation?

What if I rent my farmland — can I still get an FSFL?

Do I need crop insurance to get an FSFL?

Can I sell the grain bin before the loan is paid off?

How is the CCC rate different from other FSA loan rates?

Sources

- USDA FSA — Farm Storage Facility Loan Program

- USDA FSA — Farm Storage Facility Loan Program Fact Sheet, 2025

- USDA Economic Research Service — On-Farm Storage and Marketing, 2024