Who This Is For

Any farmer preparing to submit an FSA loan application — Direct or Guaranteed. Use this guide to assemble your documents, find your county office, and understand the timeline before your first appointment.

Who Should Look Elsewhere

Farmers applying to commercial lenders (National Funding, Fora Financial, Farm Credit) follow a different process — check each lender's review page for their specific application steps.

Before You Start

The FSA loan application process is more document-intensive than commercial lenders, but the effort is worthwhile. Direct farm ownership loans are currently available at 5.50% fixed — well below most commercial agricultural lenders. For operating loans, the current Direct rate is 5.25%.

— USDA Farm Service Agency

Watch this USDA explainer video:

The most common reason for delays is an incomplete application. Before scheduling your pre-application meeting, gather your last three years of federal tax returns (including Schedule F) and prepare a simple list of your farm assets and outstanding debts.

Walking in with organized financial records signals preparedness and speeds up your loan officer's review.

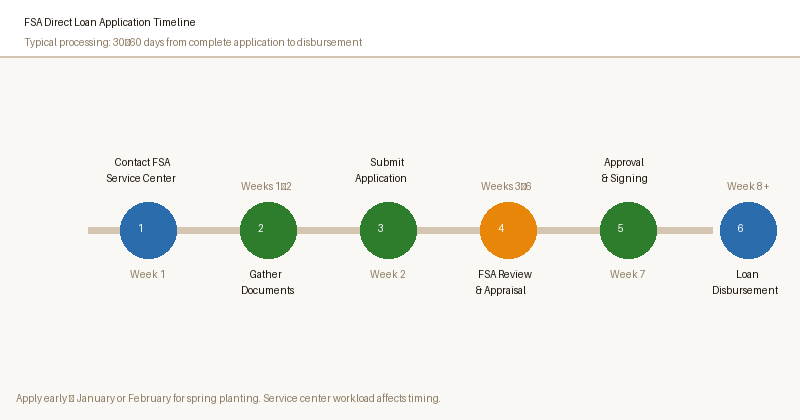

The 7-Step Application Process

-

1

Find Your County FSA Office

All FSA Direct loan applications begin at your local FSA county service center (find yours at farmers.gov). Find yours using the office locator at fsa.usda.gov by entering your ZIP code or county name. Most counties have a dedicated farm loan officer.

If you farm in multiple counties, apply in the county where the majority of your farmland is located or where you do most of your farming activity.

-

2

Schedule a Pre-Application Meeting

Call your county office and ask to schedule a pre-application meeting with the farm loan officer.

This meeting is free and not a formal application — it's a consultation where you describe your operation and financial situation, and the loan officer tells you exactly what you'll need to submit.

Bring whatever financial records you have to this first meeting. The loan officer will review them and provide a tailored document checklist. This step alone can save weeks of back-and-forth on missing items.

-

3

Gather Your Required Documents

This is the most time-consuming step. Use this checklist to make sure you have everything before submitting your formal application:

FSA Loan Application — Document Checklist

3 yearsof federal income tax returns (Schedule F — Profit or Loss from Farming)- Current farm balance sheet (assets and liabilities as of today)

- 12-month cash flow projection (income and expenses for the coming year)

- Legal description of land, equipment, or other collateral

- FSA farm number and tract records (from any prior FSA program participation)

- Government-issued photo ID (driver's license, passport)

- Statements for all existing loans (balance, lender, monthly payment)

- Proof of farming experience (prior tax returns, rental agreements, employment records)

- Denial letters from commercial lenders (for Direct loans — demonstrates "can't get credit elsewhere")

-

4

Complete

FSA Form 2001— Farm Loan ApplicationThe formal application is submitted on FSA Form 2001. Your loan officer will walk you through this form, or you can download it from fsa.usda.gov. The form collects information about you, your operation, the loan purpose, and your financial situation.

Once you submit

Form 2001with all supporting documents, FSA has a statutory obligation to notify you within 10 days whether your application is complete or if additional items are needed. -

5

Credit Evaluation and Farm Appraisal

FSA will review your credit history, verify your financial statements, and in most cases order an appraisal of the property or equipment being financed.

For farm ownership loans, a licensed real estate appraisal is required. For operating loans, FSA may appraise equipment or crops that will serve as collateral.

This step takes the most time — typically 30–60 days for Direct loans. The appraisal alone can take 2–4 weeks depending on the availability of licensed appraisers in your area. For Guaranteed loans processed through a bank, this step typically takes 2–4 weeks.

-

6

Respond to Any Additional Requests

Your loan officer may request additional documentation, clarification on your cash flow projections, or an updated balance sheet if circumstances have changed.

Respond quickly — delays in responding to FSA information requests are a leading cause of extended processing timelines.

Stay in contact with your loan officer throughout this process. A brief weekly check-in call keeps your application top of mind and signals that you're actively engaged.

-

7

Loan Closing and Disbursement

Once your loan is approved, you'll sign loan documents at your county FSA office or with your participating lender (for Guaranteed loans).

Funds are typically disbursed within a few days of closing for operating loans, or at closing for real estate transactions.

FSA will set up a repayment schedule. For operating loans, annual payments are typically due after harvest. For ownership loans, FSA will establish a monthly or annual payment schedule tied to your cash flow cycle.

Common Reasons Applications Are Denied — and What to Do

| Denial Reason | What It Means | What to Do |

|---|---|---|

| Insufficient repayment ability | Your cash flow projection shows you can't service the loan | Reduce requested loan amount; restructure repayment term; add a co-borrower |

| Prior FSA loan default | You previously defaulted on an FSA loan without settling the debt | Contact FSA to discuss debt settlement or compromise options before reapplying |

| Fails "credit elsewhere" test | FSA determined you can obtain commercial credit on reasonable terms | Request Guaranteed loan instead; provide additional evidence of commercial denials |

| Insufficient collateral | Collateral value doesn't support the loan amount requested | Reduce loan amount; identify additional collateral; consider a co-signer |

| Incomplete application | Missing documents prevented underwriting from completing | Resubmit with all required items; pre-application meeting helps prevent this |

| Citizenship/residency issue | Eligibility documentation insufficient | Provide updated immigration status documentation to your loan officer |

If your application is denied, you have the right to appeal. Request a written explanation of the denial from your loan officer, then appeal to your state FSA committee.

Appeals that are not resolved at the state level may go to the USDA National Appeals Division.

How the Guaranteed Loan Application Differs

For a Guaranteed loan, you don't apply to FSA directly — you apply to a participating commercial lender (your bank, a Farm Credit institution, or another FSA-approved lender).

The lender assesses your application according to their own credit standards, then requests a guarantee from FSA.

The documentation is similar, but your lender packages it and submits the guarantee request to FSA on your behalf. You'll work with your lender's agricultural loan officer, who knows the local FSA process.

Guaranteed loans typically close 2–4 weeks faster than Direct loans because the bank handles most of the administrative work.

Ready to Start? Find Your County FSA Office

Pre-application meetings are free and take about an hour. Bring your last 3 years of tax returns and a rough list of your farm assets and debts.

AcreCompass has no affiliate relationship with USDA.

Frequently Asked Questions

Can I start my FSA application online?

Do I need a business plan to apply for an FSA loan?

What if I don't have 3 years of farming tax returns?

How do I prepare a cash flow projection for FSA?

Can my spouse or a family member be a co-borrower?

What is an FSA farm number and do I need one?

How will I know if my application is approved?

Sources

- USDA FSA — Farm Loan Programs and Application Process

- USDA

FSA Form 2001— Farm Loan Application - USDA FSA — Beginning Farmer Resources

- farmers.gov — USDA Online Services Portal