- APH = average of your actual yields over

4–10 years(Olympic average drops highest/lowest when 10 years are available) - T-yields (transitional yields) are assigned for years with no production records — these are often lower than actual yields

- A catastrophic loss year can permanently lower your APH unless you file a yield exclusion

- You must report actual production to your crop insurance agent each year to maintain accurate APH records

- Organic crops have separate T-yields and premium factors

How APH Is Calculated

Your APH yield is determined by averaging your actual per-acre yields across the available years in your production history database (PHD). The minimum history required is 4 years; the maximum used is 10 years. When fewer than 4 years of actual yields are available, T-yields fill in the gaps.

— USDA Risk Management Agency — APH Policy Guidelines

- Actual Production History (APH)

- Your farm's historical yield average over 4-10 years, used to set your per-acre crop insurance guarantee.

- T-Yield (Transitional Yield)

- A county-based substitute yield (65-70% of county average) used for years when you have no actual production records.

- Yield Exclusion

- An option to remove years from your APH when county-wide yields fell 50% or more below the 10-year county average.

- Olympic Average

- At 10 years of history, your APH drops the highest and lowest yields and averages the remaining 8.

Pros

- Your APH is the foundation of your crop insurance guarantee — higher APH means higher coverage

- Olympic average at 10 years (drop high and low) reduces the impact of single bad years

- Yield Exclusion lets you drop disaster years when county yields fell 50%+ below trend

- APH builds over time — each good year raises your future coverage level

- Applies across all federal crop insurance products (RP, YP, RP-HPE)

Cons

- Missing years use T-yields at only 65–70% of county average — significantly lowers your APH

- Every poor yield year stays in your history for up to 10 years

- New farmers start with T-yields until they build 4+ years of actual production records

- APH cannot exceed the county reference yield (prevents over-insurance)

- Yield Exclusion is county-based — your individual bad year may not qualify if the county average held up

Who This Is For

Any farmer who buys federal crop insurance — your APH directly determines your coverage guarantee. Understanding APH is essential for maximizing your protection and knowing when to use Yield Exclusion.

Who Should Look Elsewhere

Farms using WFRP (Whole-Farm Revenue Protection) use Schedule F revenue instead of APH yields — this guide is specifically for standard crop-by-crop policy holders.

When exactly 10 years of history are available, RMA (Risk Management Agency) applies an Olympic average — dropping the single highest and single lowest year before averaging the remaining eight. For fewer than 10 years, a simple average is used.

A Real Corn Farmer Example

Suppose a corn farmer in central Illinois has the following 7-year yield history (bushels per acre):

7-Year Corn APH Calculation Example

At 80% coverage and a $4.80 corn price election: 194 × 0.80 × $4.80 = $745.73/acre guarantee

Note how the catastrophic 2021 drought year (148 bu/ac) pulls the APH down from what it would be without it (~202 bu/ac). This is why yield exclusion elections can matter significantly for farmers who experienced widespread disaster years.

T-Yields: What They Are and When They Apply

A transitional yield (T-yield) is a county-average yield assigned by RMA when a farmer lacks an actual production record for a given year. T-yields are used to fill in years where:

- You did not plant the crop in that year

- You are a beginning farmer without a full production history

- Production records are missing or cannot be documented

- The unit was newly established

T-yields are typically set at 65–70% of the county expected yield — meaning they are deliberately conservative. Every year that a T-yield appears in your APH database instead of an actual yield pulls your average down, which reduces your insurance guarantee and can push up your premium per unit of coverage.

How to Protect Your APH

Your APH is a living record that updates each year. Protecting and building it requires consistent attention at the end of each crop year:

- Report actual production every year — even in poor years, actual yields above the T-yield level improve your database over time

- Keep accurate production records — scale tickets, bin measurements, and settlement sheets support your production report

- Report on time — production reports are typically due within 60 days of harvest or the final harvest date in your county

- Review your APH database annually — ask your agent to show you the full year-by-year record and identify any T-yields that could be replaced

- Understand unit structure — basic units (by FSN and crop) versus optional units affect how yields are averaged across fields

Yield Exclusion (YE) Option: What It Is and How It Helps

The Yield Exclusion (YE) option allows farmers to exclude the yield from a catastrophic crop year from their APH calculation — but only under specific conditions. YE is available when RMA determines that a county experienced a qualifying catastrophic yield loss in a particular year.

When YE is elected for an eligible year, that year's actual yield is replaced with the simple average of the remaining years (or a T-yield, whichever is higher). This prevents a single disaster year from permanently depressing your APH guarantee.

YE Eligibility Requirements

- The county must have experienced a crop year where average county yields were at least 50% below the 10-year Olympic average for that crop

- Your farm's loss in that year must meet the threshold for your unit

- You must elect YE before the applicable sales closing date

- YE adds a small premium surcharge — typically worth it for significant catastrophic years

Check eligible YE years for your county at rma.usda.gov

RMA publishes the list of counties and crop years that qualify for Yield Exclusion. Log in to the RMA Cost Estimator or contact your crop insurance agent to see if any recent years in your county qualify. RMA agent tools →

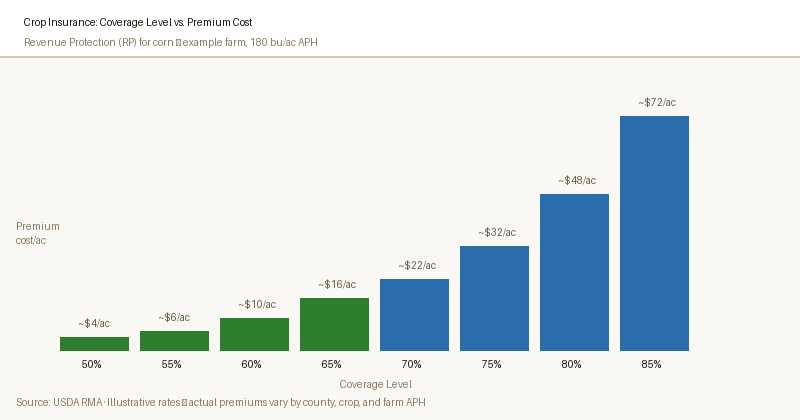

APH and Your Insurance Guarantee

Your APH is the foundation of your per-acre yield guarantee. The full formula for calculating your revenue guarantee under a Revenue Protection (RP) policy is:

Revenue Guarantee = APH Yield × Coverage Level × Price Election

For example: 194 bu/ac APH × 80% coverage × $4.80 corn price = $745.73/ac revenue guarantee. If your actual harvested revenue (yield × harvest price) falls below this level, an indemnity payment is triggered for the difference.

| APH Yield | Coverage Level | Price Election | Revenue Guarantee / Acre |

|---|---|---|---|

| 194 bu/ac | 70% | $4.80 | $652.03 |

| 194 bu/ac | 80% | $4.80 | $745.73 |

| 194 bu/ac | 85% | $4.80 | $792.58 |

| 175 bu/ac | 80% | $4.80 | $672.00 |

| 210 bu/ac | 80% | $4.80 | $806.40 |

Price elections are set by RMA at the beginning of the crop year. The above example uses a hypothetical corn price for illustration only.

Common APH Mistakes Farmers Make

- Failing to report production one year — a skipped year locks in a T-yield, often lower than your actual performance that year

- Reporting at the wrong unit level — basic vs. optional vs. enterprise units each average yields differently and affect your APH in different ways

- Not electing Yield Exclusion after a disaster year — one catastrophic year can drag down a 10-year average for nearly a decade without YE

- Assuming your APH is accurate — agents make data entry errors; review your PHD printout every year before the sales closing date

- Starting fresh fields without establishing history — newly broken ground defaults to T-yields for up to 4 years; document actual yields from the first season

Frequently asked questions

What is a T-yield and is it the same as my APH?

How many years of history do I need to have an accurate APH?

8–10 years of documented yields have the most predictable and defensible APH calculations.