Pros

- Lowest farm loan rates in the U.S. — set by Treasury, not by market negotiation

- Fixed rate for life with no prepayment penalties on any FSA loan

- Beginning farmer priority processing and dedicated funding set-asides

- No minimum credit score — FSA evaluates full financial picture

$5.8 billion issued in FY2024 to 115,000+ farmers nationwide

Cons

- Direct loans require you to prove inability to get credit elsewhere

- Processing takes 30–60 days — longer than any commercial lender

- Loan caps ($600K ownership, $400K operating) may be insufficient for large operations

- Requires in-person appointment at your local FSA Service Center

- Extensive documentation: 3 years of tax returns, balance sheet, cash flow projection, farm business plan

Who This Is For

Farmers who want the absolute lowest rate available and are willing to invest 30–60 days in the application process. Especially valuable for beginning farmers, farmers turned down by commercial lenders, and operations that benefit from long-term fixed rates.

Who Should Look Elsewhere

Large operations needing more than $600K should use FSA Guaranteed loans (up to $2.24M through a bank). Farmers who need capital within 2 weeks should apply to commercial lenders while their FSA application processes.

What Is the USDA Farm Service Agency?

Watch this USDA explainer video:

The Farm Service Agency (FSA) is a branch of the U.S. Department of Agriculture that administers farm loan programs, disaster assistance, and commodity price support for American farmers and ranchers.

FSA operates through a network of more than 2,100 county service centers across the country.

- FSA Direct Loan

- A loan made directly by the Farm Service Agency to the borrower, with no commercial bank involved. Maximum

$600,000for ownership, $400,000 for operating. - FSA Guaranteed Loan

- A loan made by a commercial lender with up to 95% of the principal guaranteed by FSA against loss. Maximum

$2,236,000. - FSA Microloan

- A simplified Direct loan up to

$50,000with reduced documentation requirements. Same rate as standard operating loans. - Credit-Elsewhere Test

- The FSA requirement that Direct loan applicants must demonstrate they cannot obtain credit from a commercial lender on reasonable terms.

In fiscal year 2024, FSA made approximately

— USDA Farm Service Agency$5.8 billion in farm loans to more than 115,000 farmers and ranchers — making it one of the largest agricultural lenders in the United States. FSA is not a lender of last resort; it is designed to serve farmers who are unable to obtain credit from commercial sources on reasonable terms, as well as beginning and underserved farmers.

Types of FSA Loans

FSA administers five main loan types. Each serves a distinct purpose and has its own maximum loan amount, interest rate, and repayment term.

| Loan Type | Purpose | Max Amount (Direct) | Rate | Max Term | Best For |

|---|---|---|---|---|---|

| Farm Ownership Loan | Buy, expand, or improve farmland | $600,000 |

5.50% | 40 years | Buying land or farm real estate |

| Operating Loan | Seeds, inputs, livestock, operating expenses | $400,000 |

5.25% | 7 years | Annual crop production expenses |

| Emergency Loan | Disaster recovery — drought, flood, fire | $500,000 |

Varies | Up to 40 years | Farmers in presidentially declared disaster areas |

| Microloan | Small operating needs, new farmers | $50,000 | 5.25% | 7 years | Beginning farmers, niche operations |

| Farm Storage Facility Loan | Grain bins, silos, cold storage | $500,000 | ~2.5% (CCC) | 12 years | On-farm commodity storage |

FSA Direct vs. Guaranteed Loans: Key Differences

Every FSA loan type except Emergency loans is available in two forms: Direct or Guaranteed. Understanding the difference is critical to choosing the right application pathway.

Direct loans come directly from USDA — the federal government is your lender, and you make payments to FSA.

Direct loans carry the lowest rates but have strict eligibility requirements, including demonstrating that you cannot obtain credit elsewhere on reasonable terms. Application and processing happen at your county FSA office.

Guaranteed loans come from a private bank or commercial lender, with USDA guaranteeing up to 95% of the loan amount. You work with your lender — not FSA — to apply.

The bank absorbs 5% of the risk. Guaranteed loans can be larger (up to $2.24 million), close faster, and do not require proving you lack access to commercial credit.

For a full comparison, see our FSA Direct vs. Guaranteed Loans guide.

Who Qualifies for FSA Loans

Eligibility requirements vary by loan type, but all FSA loans share several base criteria:

- U.S. citizenship or legal residency — permanent resident aliens are eligible

- Farm history or experience — at least 1 year of farming experience (or agricultural college education) for most loan types

- Acceptable credit history — FSA does not set a minimum credit score, but reviews your entire credit history; consistent delinquency or prior FSA loan default can disqualify you

- Legal capacity — ability to incur the obligation of a loan

- "Unable to obtain credit elsewhere" (Direct loans only) — you must demonstrate that commercial lenders have declined your application or offered only unreasonable terms

Beginning farmers — defined as those with fewer than 10 years of farming experience — receive priority for Direct loans. FSA reserves a portion of each year's loan funding specifically for beginning and socially disadvantaged farmers.

Current FSA Loan Rates (May 2026)

FSA loan rates are set quarterly by the USDA and tied to the cost of government borrowing. They typically run significantly below commercial bank rates for agricultural lending.

| Loan Type | Current Rate | Last Changed | Rate Type |

|---|---|---|---|

| Direct Farm Ownership | 5.50% | Feb 2026 | Fixed |

| Direct Farm Operating | 5.25% | Feb 2026 | Fixed |

| Direct Emergency Loan | 3.75% | Feb 2026 | Fixed |

| Microloan (Operating) | 5.25% | Feb 2026 | Fixed |

| Farm Storage Facility | ~2.50% | Apr 2026 | CCC rate |

| Guaranteed Loans | Negotiated with lender | Ongoing | Fixed or variable |

Rates update quarterly. Verify current rates at fsa.usda.gov before applying.

How to Apply

All FSA Direct loan applications begin at your local county FSA service center. For Guaranteed loans, you apply through a participating commercial lender — your bank contacts FSA to request the guarantee.

Documents typically required for a Direct loan application:

- 3 years of federal income tax returns (Schedule F)

- Current balance sheet (assets and liabilities)

- 12-month cash flow projection

- Legal description of property, equipment, or other collateral

- FSA farm number and tract records

- Government-issued photo ID

- Statements for any existing loans

For a step-by-step walkthrough, see our How to Apply for a USDA Farm Loan guide.

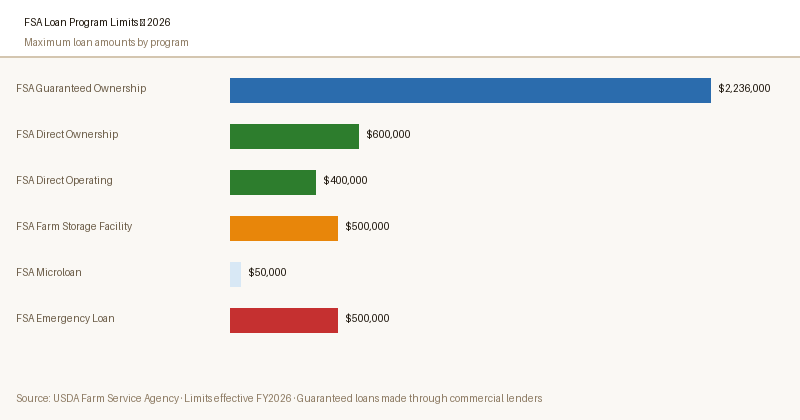

FSA Loan Limits Table

| Loan Type | Direct Limit | Guaranteed Limit | Lifetime Limit |

|---|---|---|---|

| Farm Ownership | $600,000 | $2,236,000 | $600,000 direct |

| Operating | $400,000 | $2,236,000 | $400,000 direct |

| Emergency | $500,000 | N/A | N/A |

| Microloan | $50,000 | N/A | $50,000 |

| Farm Storage Facility | $500,000 | N/A | N/A |

Loan limits are set by Congress and subject to periodic adjustment. Combined Direct loans (all types) cannot exceed $600,000 in aggregate outstanding principal.

Ready to Apply for an FSA Loan?

Visit the USDA FSA website to find your county office, download application forms, and check current rates.

Visit USDA FSA →AcreCompass has no affiliate relationship with USDA. We link to FSA because they offer farmers the lowest available rates.

Frequently Asked Questions

What is the minimum credit score for an FSA loan?

How long does an FSA loan take to process?

Can I have both a Direct and a Guaranteed FSA loan?

What does "unable to obtain credit elsewhere" mean?

Do FSA loans require a down payment?

Are FSA loan rates fixed or variable?

What if my FSA loan application is denied?

Do FSA loans have prepayment penalties?

Sources

- USDA Farm Service Agency — Farm Loan Programs

- USDA Economic Research Service — Agricultural Finance Monitor, 2025

- Kansas City Federal Reserve Bank — Agricultural Finance Databook, Q1 2026

- USDA FSA — Annual Report of Farm Loan Activity, FY2024