Pros

- FSA Direct operating rate (5.25%) is the lowest available for seasonal capital

- Operating loans cover all production costs: seed, fertilizer, labor, insurance premiums

- FSA Microloans ($50K) have simplified paperwork for smaller operations

- Annual renewal structure matches agricultural production cycles

- Online lenders offer 24-hour funding for urgent seasonal needs

Cons

- FSA processing takes 30–60 days — too slow for last-minute planting needs

- Commercial operating rates (7–24%+) are significantly higher than FSA

- Annual renewal means reapplication and re-qualification every year

- FSA requires inability to get credit elsewhere — not everyone qualifies

- Over-borrowing on operating loans is the #1 cause of farm financial distress

Who This Is For

Any farmer who needs capital for seasonal production costs — seeds, fertilizer, crop chemicals, livestock feed, hired labor, and insurance premiums.

Beginning farmers should apply for FSA Direct first; established operations typically use Farm Credit or bank operating lines.

Who Should Look Elsewhere

Farmers purchasing land or equipment should use ownership or equipment-specific loans with longer terms and lower rates. Operations with strong cash reserves may not need an operating loan at all.

What Does a Farm Operating Loan Cover?

Watch this USDA explainer video:

Farm operating loans are designed to bridge the gap between the start of the production season and the sale of your crop or livestock.

Unlike a land loan or equipment loan, operating financing is consumed in the course of production — it doesn't create a durable asset on your balance sheet.

Eligible uses for farm operating loan proceeds include:

- Seed and planting costs — Corn, soybean, wheat, cotton, vegetable, and specialty crop seed, plus cover crop seed

- Fertilizer and lime — Anhydrous ammonia, UAN solutions, phosphorus, potassium, and soil amendments

- Pesticides and herbicides — Pre-emergent and post-emergent crop protection, fungicide applications

- Fuel and lubricants — Diesel and propane for tractors, combines, grain dryers, and irrigation pumps

- Crop insurance premiums — MPCI (Multi-Peril Crop Insurance), revenue protection, and supplemental coverage insurance premiums

- Hired labor and custom farming — Seasonal workers, planting contractors, and custom harvesting fees

- Livestock feed and veterinary costs — Corn, soy meal, hay, and veterinary care for beef, dairy, and swine operations

- Machine rental and lease payments — Short-term equipment rental during peak planting or harvest

- Irrigation water costs — Canal fees, water district assessments, and power for pumping

$180/acre expected gross revenue, a lender might size your line at $126,000–$144,000. FSA uses a cash flow budget rather than a simple percentage.FSA Farm Operating Loans

The USDA Farm Service Agency offers two types of operating loans that represent the most affordable option for most farmers who qualify.

FSA Direct Operating Loans

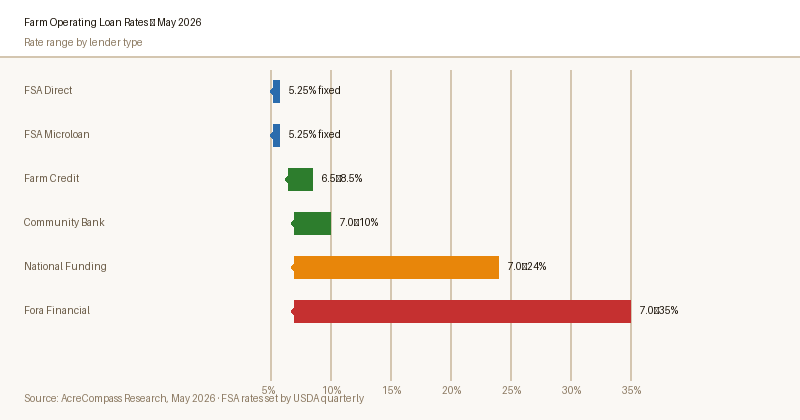

FSA Direct Operating Loans are funded directly by the federal government through your local FSA service center. As of May 2026, the interest rate is 5.25%, adjusted monthly based on USDA's cost of funds. Key parameters:

— USDA Farm Service Agency

- Maximum loan amount:

$400,000 - Maximum term: 7 years for annual operating; terms may be extended for multi-year crops

- Collateral: All available collateral is required — growing crops, equipment, real estate

- Who qualifies: Farmers who are unable to obtain credit at reasonable rates from commercial sources

- Beginning farmer priority: FSA reserves a portion of direct operating loan funds specifically for beginning farmers

FSA Microloans

For smaller operations, the FSA Microloan program offers up to $50,000 with a streamlined application process that doesn't require a full financial history. Microloans are designed for small and beginning farmers, veterans, and those in underserved communities.

The application is significantly simpler than a standard FSA loan, making it an excellent entry point for new farmers. The rate is the same as the standard direct operating loan rate: 5.25% as of May 2026.

USDA FSA Operating Loans — No Affiliate Relationship

AcreCompass has no affiliate relationship with USDA. Apply for FSA operating loans at fsa.usda.gov or contact your local FSA service center. Processing typically takes 30–60 days.

Commercial Operating Loans

When FSA processing timelines don't fit your planting season calendar — or when your operation doesn't qualify for FSA programs — commercial lenders offer faster alternatives at higher rates.

National Funding

National Funding is the fastest commercial option for farm operating capital. They approve loans up to $500,000 based primarily on recent business revenue, with decisions in 24 hours and funding in 1–3 business days.

Their agricultural lending product is a term loan rather than a revolving line, which works well for one-time seasonal capital needs. Starting rates are approximately 7.00%, with effective APR (annual percentage rate) depending on loan term and credit profile. Minimum time in business: 2 years. Minimum monthly revenue: approximately $20,000.

Fora Financial

Fora Financial lends up to $1.4 million on agricultural operating needs, with less emphasis on collateral than traditional banks. They evaluate recent business performance heavily — six months of bank statements typically replaces years of tax return analysis.

This makes Fora Financial particularly useful for operations that have grown rapidly or recently restructured ownership. Rates range from approximately 7.00% to 35% depending on risk profile, with funding in 24–72 hours.

Farm Operating Line of Credit vs. Seasonal Note

The two most common structures for farm operating financing differ in how they're drawn and repaid:

A revolving line of credit works like a business credit card — you borrow up to your limit, repay, and borrow again within the same production year. Interest accrues only on outstanding balances.

Community banks and Farm Credit institutions typically offer revolving lines, which are ideal for operations with staggered expense timing across multiple crops or livestock cycles.

A seasonal note (or crop production loan) is a single advance at the start of the season, repaid in full at harvest.

FSA operating loans are typically structured as seasonal notes. This structure is simpler to administer but less flexible if your cash needs are variable throughout the year.

Current Operating Loan Rates — May 2026

| Lender | Rate | Max Loan | Term | Funding Speed | Apply |

|---|---|---|---|---|---|

| FSA Direct | 5.25% | $400K | 1–7 yr | 30–60 days | Visit FSA → |

| FSA Microloan | 5.25% | $50K | 1–7 yr | 30–60 days | Visit FSA → |

| Farm Credit | 6.5–8.5% | Varies | 12 mo revolving | 1–3 weeks | Apply → |

| National Funding | 7.00–24% | $500K | 2–5 yr | 1–3 days | Apply → |

| Fora Financial | 7.00–35% | $1.4M | 4–15 mo | 24–72 hrs | Apply → |

| Lendio | Varies | $5M | Varies | 2–7 days | Apply → |

Affiliate disclosure: Commercial lender links may earn AcreCompass a commission. FSA links are not affiliate links. Rates as of May 2026.

Need Operating Capital Fast? National Funding Approves in 24 Hours

Don't let planting season pass while waiting for a bank decision. National Funding approves operating loans up to $500K within 24 hours — no collateral required for qualified borrowers.

Check Rates at National Funding →How to Apply for an FSA Operating Loan

-

1Contact your local FSA service centerFind your county service center at fsa.usda.gov. Call ahead to schedule a pre-application meeting — this helps you understand local processing timelines and specific documentation requirements.

-

2Prepare your financial documentsGather 3 years of Schedule F tax returns (or business tax returns for farm corporations), a current farm balance sheet listing assets and liabilities, crop insurance certificates, and a current operating plan with projected income and expenses.

-

3Complete

FSA Form 2001The FSA Loan Application (Form 2001) captures your farm description, loan purpose, requested amount, and legal entity information. Your loan officer will guide you through this form at your service center appointment. -

4FSA underwrites and appraises collateralFSA will review your application, conduct a credit check, and appraise any collateral you're pledging. For operating loans, the growing crop itself is typically the primary collateral. This step takes 2–4 weeks.

-

5Receive approval and sign loan documentsIf approved, you'll sign the promissory note and security agreement at your service center. FSA disburses funds directly to your farm account or, for certain expenses, directly to suppliers.

Frequently Asked Questions

What is the FSA operating loan interest rate in 2026?

How long does FSA take to approve an operating loan?

Can I get an operating loan if I've been turned down by my bank?

Do operating loans require crop insurance?

What's the difference between an operating loan and a line of credit?

Can I use an operating loan to pay rent on farmland?

How is an operating loan repaid?

Sources

- USDA Farm Service Agency — Operating Loan Programs, rates verified May 2026

- USDA Economic Research Service — Farm Income and Finance: Farm Business Balance Sheet, 2025

- Federal Reserve Bank of Kansas City — Agricultural Finance Databook, Q1 2026

- USDA NASS (National Agricultural Statistics Service) — Farm Production Expenditures Survey, 2025